Happy Friday!

In this week’s letters,

– Fawkes Capital Management on German infrastructure and AI war;

– Ameliora Wealth Management on the US debt burden, European equities;

– 49 Financial on Tariff-Induced Volatility and Middle East Conflict

– Elevator pitches for SWX; IQV; APPF;

Quarter in progress: 639 fund letters of Q2 are live on our database!

Want to know what BSDs are buying (or selling)?

We just launched the BSD 13Fs Investor Page, your new central hub to:

![]() Search BSD Gurus by name, portfolio value, or ticker

Search BSD Gurus by name, portfolio value, or ticker

![]() Track 13F filings from 100+ top hedge funds and BSDs

Track 13F filings from 100+ top hedge funds and BSDs

![]() Compare turnover rates, holdings, and portfolio shifts

Compare turnover rates, holdings, and portfolio shifts

![]() Spot new positions and high-conviction moves instantly

Spot new positions and high-conviction moves instantly

From David Einhorn to Warren Buffett, their most important filings are now all in one place — simplified, visual, and always up-to-date.

Enjoy fishing for ideas!

Q2 2025 INVESTOR LETTER SUMMARIES

- German Infrastructure – Our investments here are unchanged with Friedrich Vorwerk showing significant earnings momentum in Q2. The company cited the potential for far more significant growth as a result of the hydrogen energy pipeline plan the German Cabinet recently passed.

- Western AI beneficiaries – The next iteration of NVIDIA’s GPU architecture, Rubin, is scheduled for release in 2026 and is set to significantly alter the energy infrastructure within data centres.

- Chinese AI Development – It is becoming increasingly clear that the Chinese Communist Party (CCP) views the AI race as existential. Just as the Space Race defined global power dynamics in the 20th century, the AI race may determine which nations project influence in the 21st century.

- The U.S. debt burden, now above 120% of GDP in connection with a current budget deficit expected to be around 7% of U.S. output, is weighing heavily on the currency. Many prognosticators, such as Morgan Stanley and JPMorgan, are forecasting a further 10% drop in the dollar by year-end or within the next 12 months.

- European equities outperformed their U.S. counterparts over the last 6 months, both in local and USD terms. We could argue that this big move was supported by cheaper valuations, the big infrastructure and defense spending spree, but it could also be a revert to the mean after U.S. markets massively outperformed Europe in the previous years.

- In our opinion, there are several reasons to remain cautious. Our focus remains on non-US investments until there is more clarity on tariffs, the final passing of the tax bill currently being discussed in Congress, and the potential for renewed military conflict in the Middle East.

- Tariff-Induced Volatility and Relief Rally – The quarter opened with markets under pressure as renewed trade tensions raised fears of higher tariffs, supply chain disruptions, and slowing global growth—especially in manufacturing, technology, and consumer sectors.

- Rising Conflict in the Middle East – Geopolitical tensions in the Middle East added a new layer of complexity to the global outlook. The conflict has had a multi-faceted impact on markets: Energy Markets: Oil prices fluctuated amid fears of supply disruptions and concerns about global demand. Defense and Security: Increased investor interest in defense contractors, cybersecurity firms, and energy infrastructure.Risk Sentiment: Heightened risk aversion prompted intermittent flights to safety, reinforcing the importance of a well-diversified investment approach.

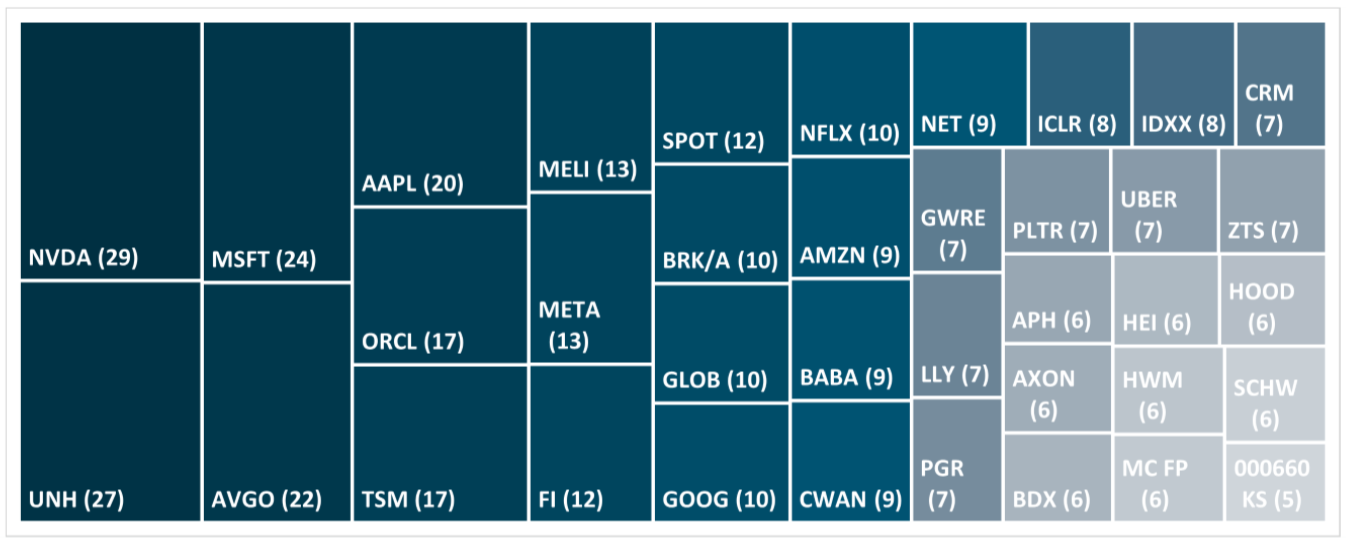

Q2 2025 TICKER TREEMAP

This quarter’s treemap of mentioned tickers (by Count)

ELEVATOR PITCHES BY FUNDS

![]()

Southwest Gas Holding (by Silver Beech Capital)

- Catalyst 1: Deconsolidation. The Path to a Pure-Play Utility – As of the second quarter, SWX holds a ~52% stake in Centuri, requiring the consolidation of Centuri’s financials. This accounting treatment masks the financials of the core utility.

- Catalyst 2: Deleveraging. Fortifying the Balance Sheet – The proceeds from Centuristock sales are being deployed in a shareholder-friendly manner.

- Catalyst 3: Understated Rate Base Growth. Market-Leading Growth – The core utility operates in prime service territories characterized by robust population growth and accelerating demand for natural gas.

- Catalyst 4: Enhanced Profitability. Improving Regulatory Landscape.

![]()

IQVIA Holdings (by Broyhill Asset Management)

- IQVIA is the result of the 2016 combination of Quintiles(a Chapel Hill-based contract research organization, or CRO)with IMS Health (a top healthcareInformation Services provider).

- IQV facilitates scientific research while focusing on later-stage trials and generating a meaningful amount of profits from its technology and data business. We view this as an entrenched, high-quality revenue stream whose scale and network effects afford it an advantage against smaller peers.

- Despite this, shares still bottomed at 11x forward earnings, and the valuation remains below historical levels.

![]()

AppFolio, Inc (by Seeking Winners)

- AppFolio’s technical sophistication is considered multiple times better than competitors. This stems from a product-led and R&D-led approach, with significant investment in building out products.

- Strategically, AppFolio is also considered better than competitors, conducting extensive market research and maintaining a strong internal strategy function that works closely with the executive team.

- AppFolio is anticipated to show re-accelerated Value Added Services growth in their upcoming Q2 2025 report. This comes after a period of VAS deceleration in Q1, which concerned investors.

- At about 26x 2026 FCF, we think the setup is solid here for AppFolio moving forward.

MEDIA APPEARANCES BY BSDst

-

-

-

-

-

- I think that what is happening now politically and socially is analogous to what happened around the world in the 1930-40 period.

- I am just describing the cause and effect relationships that are driving what is happening. And by the way, during such times most people are silent because they are afraid of retaliation if they criticise.

- A politically weakened central bank, pressed to keep rates low would undermine the confidence in the Fed defending the value of money and make holding dollar-denominated debt assets less attractive which would weaken the monetary order as we know it.

-

-

-

-

-

-

-

-

-

- I downgrade my terminology from bubble to “hey that’s an expensive market maybe we should expect a little less”. Similarly in the aggregate stock market there’s a high Schiller cape but nowhere near the peaks we’ve we’ve seen before.

- The world is not very well approximated by a normal distribution. Some things are better approximated. Five-year average returns for the major asset classes don’t look too bad.

- The sin is not having beta. The sin is charging alpha prices for beta. Having beta can actually be very useful.

-

-

-

-

-

-

-

-

-

- What the populists are doing to me has a lot of real value. What they’re doing is they’re listening to people. They’re addressing actual problems on the ground that Americans are experiencing.

- But if all the benefits of that growth are going to Elon Musk, who at my understanding has a net worth more than the bottom half of Americans put together. That’s not okay. Who cares about growth if it’s only going to a bunch of rich people?

-

-

-

-