Happy Friday!

In this week’s letters,

– Myrmikan Research on the value of Gold;

– 49 Financial on the main risks of 2026;

– Laughing Water Capital on the current market situation;

– Elevator pitches for ADEA; PAYC; TSCO;

Quarter in progress: 223 fund letters of Q4 are live on our database!

Want to know what BSDs are buying (or selling)?

We just launched the BSD 13Fs Investor Page, your new central hub to:

![]() Search BSD Gurus by name, portfolio value, or ticker

Search BSD Gurus by name, portfolio value, or ticker

![]() Track 13F filings from 100+ top hedge funds and BSDs

Track 13F filings from 100+ top hedge funds and BSDs

![]() Compare turnover rates, holdings, and portfolio shifts

Compare turnover rates, holdings, and portfolio shifts

![]() Spot new positions and high-conviction moves instantly

Spot new positions and high-conviction moves instantly

From David Einhorn to Warren Buffett, their most important filings are now all in one place — simplified, visual, and always up-to-date.

Enjoy fishing for ideas!

Q4 2025 INVESTOR LETTER SUMMARIES

- Gold Measures the Real Value of other Assets – We’ve already shown that gold is not volatile at all when used to measure assets: pricing assets and commodities in terms of gold reduces volatility, which is practical confirmation of Carl Menger’s theoretical deduction that gold should behave as the best money. We’ll admit, of course, that it makes less sense to look at retail prices through the gold lens: the value of bread is not jumping up and down by large percentages each week; the value of bread did not get cut in half over the past eighteen months.

- This is why industrial commodities did not keep up with gold in the 1970s, preserving gold mining margins. We think similar dynamics are at play again, with two major outliers: oil and silver.

- Given the Trump administration’s increasingly aggressive foreign policy dedicated towards capturing resources for aligned countries, global manufacturers are losing trust in contracts for future delivery and are aggressively stockpiling resources.

- De-globalization and elevated geopolitical risk: The global economy is shifting from decades of integration toward regionalization. Trade fragmentation, supply-chain realignment, rising defense spending, and persistent geopolitical tensions are no longer episodic risks; they are structural features of the investment landscape.

- Concentration risk in passive benchmarks: Concentration risk within U.S. equity benchmarks has reached extreme levels. More than 40% of the S&P 500’s market capitalization is now represented by just eight companies.

- U.S. dollar devaluation: The U.S. dollar showed renewed signs of structural weakness in 2025, driven by persistent fiscal deficits, shifting interest-rate dynamics, and evolving global capital flows.

- Elevated Valuations and Suppressed Volatility – U.S. equity valuations remain elevated, while market volatility remains unusually subdued given the macro and geopolitical risks present.

- I am not calling a bubble in these matters, but I am comfortable saying there is a fair bit of enthusiasm. By contrast, over shorter periods we are more likely to have the crowd question our sanity than we are to benefit from the madness of crowds.

- Admittedly, our lead versus the S&P 500 Total Return Index (SP500TR) has narrowed quite a bit in recent years. Ultimately, our success will depend on my ability to pick individual stocks that outperform, so I cannot blame the environment entirely for this narrowing. However, the environment is at least worth being aware of.

- Take, for example, our investment in Lifecore Biomedical, our CDMO that puts injectable drugs into syringes and vials. I have written about this investment extensively in the past, but, in brief, Lifecore has excess capacity in a market where there is a global shortage of capacity, demand is growing, and new supply cannot be quickly or effectively built because of a constrained supply chain and regulatory barriers.

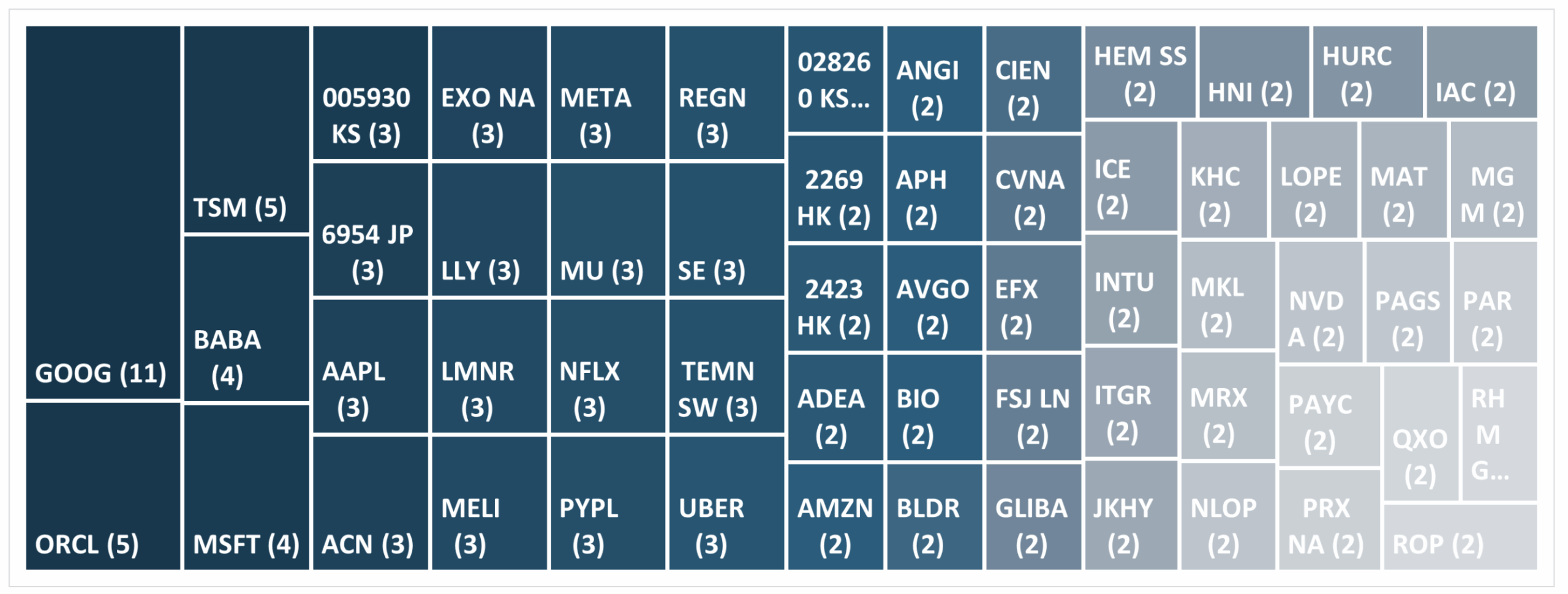

Q4 2025 TICKER TREEMAP

This quarter’s treemap of mentioned tickers (by Count)

ELEVATOR PITCHES BY FUNDS

![]()

Adeia Inc. (by Riverwater Value Strategy)

- We initiated a position in Adeia, Inc. (ADEA) in the fourth quarter. ADEA licenses intellectual property (IP) to its customers for use in their media and semiconductor products and services.

- Spun out of Xperi Inc. in 2022, ADEA has a broad range of media customers as licensees. Additionally, hybrid bonding is becoming a key technology used by semiconductor manufacturers as complexity increases. ADEA’s IP is currently licensed by the major memory players, with several logic players also interested.

- As media delivery and semiconductor complexity increase, IP relevance rises, not falls. This is not a growth darling, but it doesn’t need to be.

![]()

Paycom Software (by Spheria Global)

- PAYC provides cloud-based human capital management (HCM) software for small to mid-sized companies in the USA.

- Labour cost reduction is the biggest single source of value, which is achieved thanks to the company’s unified technology stack.

- PAYC continues to focus on the controllables, recently launching an AI-powered feature that allows users to instantly access HR and payroll data simply by asking for it in natural language. In addition, the business has a net cash balance sheet and is well placed to generate further market share gains in the medium term.

![]()

Tractor Supply Co. (by Wedgewood Partners)

- Tractor Supply detracted from performance despite +7% sales growth and +6% operating income growth. Management completed several long-term infrastructure investments. Approximately 80% of sales come from loyalty program members. We expect accelerating earnings growth in 2026 as investment spending laps. Normalization of customer spending patterns should further support results.

- Store expansion and distribution efficiency provide long-run growth levers. When consumers trade down, Tractor Supply often benefits because it sells practical value. This is a defensive retailer with real compounding characteristics.

HIGHLIGHT OF THIS WEEK

MEDIA APPEARANCES BY BSDs

-

-

-

-

-

- The US will likely slide into a small recession at the end of the year and the stock market will drop as average-income consumers struggle with high living costs.

- By the end of the year, we will have a small recession. Wealthy consumers are doing really great, going on cruises, going to Vegas, going on and spending money on all kinds of exciting things. But the average consumer is really struggling.

- Rogers said he continues to bet on small cap companies, citing Smucker Co. as one of the stocks that does well in tough economic times.

-

-

-

-

-

-

-

-

-

- In a since-deleted X post, the hedge fund billionaire said late on Friday that Trump’s call for a 10% cap on credit card interest for one year was a “mistake” that could lead to millions having their cards canceled.

- This is a mistake President,” Ackman wrote. “Without being able to charge rates adequate enough to cover losses and to earn an adequate return on equity, credit card lenders will cancel cards for millions of consumers who will have to turn to loan sharks for credit at rates higher than and on terms inferior to what they previously paid.

-

-

-

-

-

-

-

-

-

- Buffett, who recently stepped down as Berkshire’s CEO after more than 50 years in the role, said he couldn’t find any stocks or businesses that were attractively valued and large enough to move the needle at his $1 trillion conglomerate. Berkshire was only “buying one or two things, but it’s peanuts,” he said.

- But I’m willing to spend $100 billion this afternoon. I rather have $100 billion in a really good business model at a sensible price than have $100 billion in cash.

- Buffett said that holding some cash was necessary, comparing it to “oxygen” and saying you “always need to have it available because you do not know what will happen”.

-

-

-

-