Happy Friday!

In this week’s letters,

– Hinde Group on the economy and inflation;

– Doubleline Capital on the markets and credits;

– Alpine Capital on the AI, Europe, and the FED;

– Elevator pitches for ARE; SLVM; LIN;

Quarter in progress: 746 fund letters of Q4 are live on our database!

Want to know what BSDs are buying (or selling)?

We just launched the BSD 13Fs Investor Page, your new central hub to:

![]() Search BSD Gurus by name, portfolio value, or ticker

Search BSD Gurus by name, portfolio value, or ticker

![]() Track 13F filings from 100+ top hedge funds and BSDs

Track 13F filings from 100+ top hedge funds and BSDs

![]() Compare turnover rates, holdings, and portfolio shifts

Compare turnover rates, holdings, and portfolio shifts

![]() Spot new positions and high-conviction moves instantly

Spot new positions and high-conviction moves instantly

From David Einhorn to Warren Buffett, their most important filings are now all in one place — simplified, visual, and always up-to-date.

Enjoy fishing for ideas!

Q4 2025 INVESTOR LETTER SUMMARIES

- The battle with post-pandemic inflation is officially over. In both November and December, the annualized six-month change in the Fed’s preferred inflation gauge, the price index for personal consumption expenditures excluding food and energy (core PCE), came in at 1.9%.

- The picture is even clearer when housing is removed from the equation. The price index for core PCE excluding housing increased at just a 1.0% annualized rate over the second half of 2023, which is well below the Fed’s target.

- In November and December, the yield on the two-year U.S. Treasury fell from 5.07% to 4.23%. This decline reflected expectations that the Fed would soon pivot from tight monetary policy toward a more balanced stance.

- 2025 was a fantastic year for those invested in the public markets, with roaring equity performance and strong fixed-income returns across geographies and sectors. In China, 2025 was marked by on-again, off-again trade negotiations with the United States. Those negotiations included a face-to-face meeting between President Donald Trump and President Xi Jinping on the sidelines of the October APEC Summit in South Korea, which was the first such meeting since 2019.

- More broadly, 2025 challenged many traditional economic assumptions and models. The year was marked by elevated volatility driven by government policy, including tariffs and a federal shutdown.

- An anticipated inflation spike tied to the unexpected tariff regime never materialized. Instead, many companies heavily frontloaded inventories to mitigate the impact on corporate earnings, which contributed to sharp swings in quarter-over-quarter GDP growth projections.

- AI 2.0: Global Abundance. The shift from software to physicals. Our optimism regarding technology remains undiminished, but we are adapting our tactical focus to meet the next phase of development. We believe we are entering “AI 2.0,” a period in which artificial intelligence begins to foster a state of global abundance.

- Europe and Emerging Markets. Navigating the “American Bully” and the EM catch-up. The surge in Emerging Markets (EM) has been a standout feature of 2025, yet it brings a complex set of questions for the long-term investor.

- The Federal Reserve: A shifting mandate and the path to lower rates. The Federal Reserve currently stands at a crossroads, navigating the difficult “dual mandate” of maintaining price stability while ensuring maximum employment. We have frequently highlighted the precarious juxtaposition the Fed finds itself in.

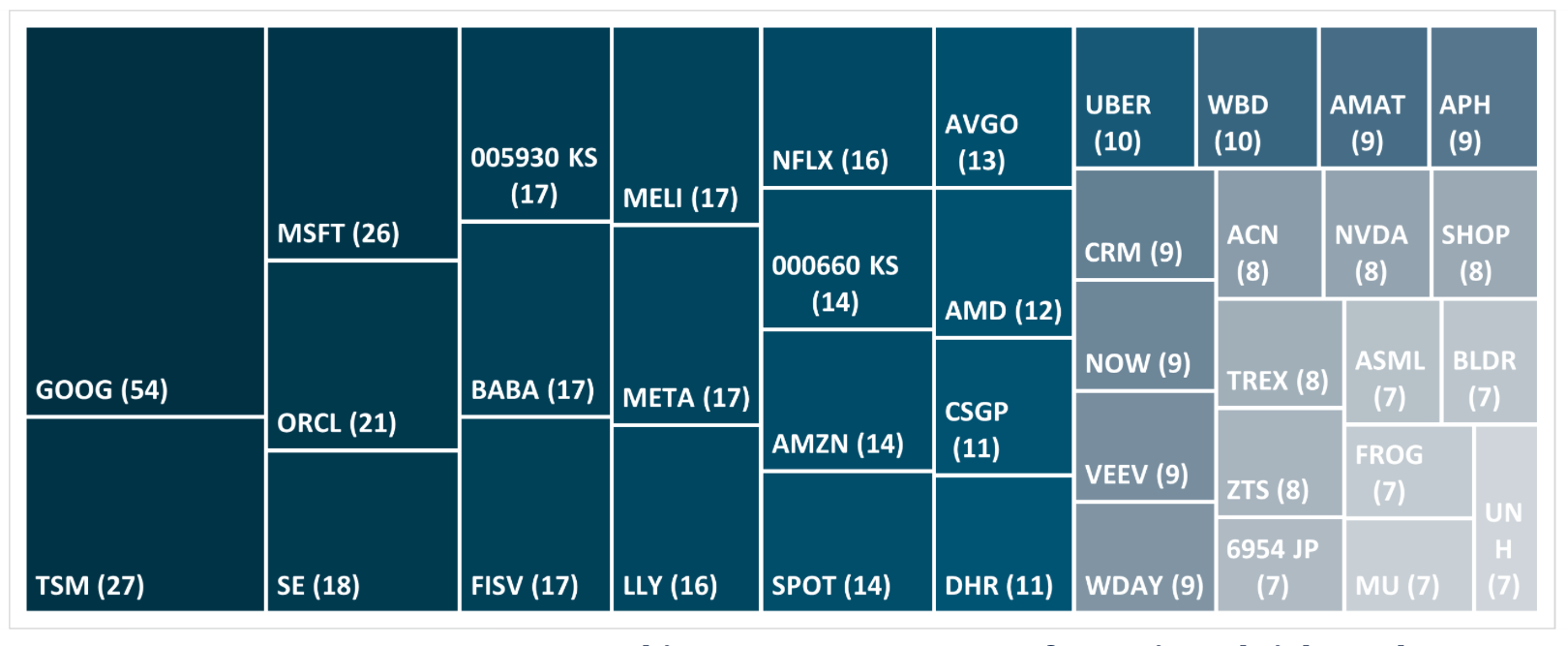

Q4 2025 TICKER TREEMAP

This quarter’s treemap of mentioned tickers (by Count)

ELEVATOR PITCHES BY FUNDS

![]()

Alexandria Real Estate (by Warden Capital)

- ARE is the largest life sciences landlord in the US – this sector has struggled with a double whammy of a biotech bust and big oversupply (triple if you want to count WFH, though lab space wasn’t hit quite as hard as normal office in this regard). I believe the stock is currently oversold – their portfolio is by far the highest quality with some truly top tier assets.

- The bio sector is coming back, and I believe strongly in its long term growth. In fact it began to recover somewhat in 2025, just take a look at the XBI.

- ARE is trading at an ~10%+ cap rate today, which I believe falls to low 9s on future NOI declines – too cheap given the strong lease terms & asset quality.

![]()

Sylvamo Corporation (by Alluvial Capital)

- In the fourth quarter, Alluvial Fund purchased shares of Sylvamo Corp, a manufacturer of uncoated freesheet paper. Sylvamo has a strong history of profitability and free cash flow generation but is facing short-term headwinds from lower paper pricing, weak European demand, and the expiration of a long-term supply agreement.

- The company is investing in its South Carolina mills to replace lost supply and increase capacity. Industry supply reductions should support pricing. Management expects the investment program to generate a 30%+ IRR and return Sylvamo to $300 million in annual free cash flow by 2027.

![]()

- The industry benefits from powerful economies of scale, physics-driven efficiency advantages, and prohibitive transportation costs that require dense, localized distribution networks. Long-term take-or-pay contracts with cost pass-through provisions create inflation-protected, utility-like cash flows.

- Despite these strengths, Linde’s shares were pressured by a global industrial slowdown, which we believe caused investors to over-discount the business as near-term “dead money.” We view this as a market-timing mispricing in a high-quality compounder with durable pricing power and long-term volume growth.

HIGHLIGHT OF THIS WEEK

MEDIA APPEARANCES BY BSDs

-

-

-

-

-

- Greenlight Capital’s David Einhorn anticipates the Federal Reserve will issue more interest rate cuts this year than what’s being anticipated and that’s giving him greater confidence in his gold bet.

- If we have 4% or 5% inflation, sure, then he won’t be able to persuade people, but otherwise he’s going to argue productivity. I think by the time we get to the end of the year, it’s going to be substantially more than two cuts.

-

-

-

-

-

-

-

-

-

- Billionaire investor Bill Ackman told clients on Wednesday that his hedge fund bought shares in Meta Platforms (META.O), opens new tab late last year, betting the technology giant will benefit from artificial intelligence.

- We believe Meta’s current share price underappreciates the company’s long-term upside potential from AI and represents a deeply discounted valuation for one of the world’s greatest businesses.

-

-

-

-

-

-

-

-

-

- Pfizer (PFE.N), opens new tab agreed to accept $29 million to resolve a dispute with the U.S. Securities and Exchange Commission stemming from the regulator’s 2013 insider trading settlement with billionaire Steven A. Cohen’s former hedge fund SAC Capital Management.

- The proposed payment disclosed in a Tuesday court filing represents nearly two-fifths of the $75.2 million left over from SAC’s $601.8 million settlement over trades in drugmakers Wyeth and Elan by Mathew Martoma, a former SAC employee who was later convicted of securities fraud and conspiracy. The U.S. Treasury would get the remaining $46.2 million.

-

-

-

-