Happy Friday!

In this week’s letters,

– The D. E. Shaw Group on the markets and the economy;

– Semper Augustus on investment and the market history;

– Hayden Capital on AI Scare and AI cycle;

– Elevator pitches for TVE CN; IHS; OXY

Quarter in progress: 771 fund letters of Q4 are live on our database!Want to know what BSDs are buying (or selling)?

We just launched the BSD 13Fs Investor Page, your new central hub to:

![]() Search BSD Gurus by name, portfolio value, or ticker

Search BSD Gurus by name, portfolio value, or ticker

![]() Track 13F filings from 100+ top hedge funds and BSDs

Track 13F filings from 100+ top hedge funds and BSDs

![]() Compare turnover rates, holdings, and portfolio shifts

Compare turnover rates, holdings, and portfolio shifts

![]() Spot new positions and high-conviction moves instantly

Spot new positions and high-conviction moves instantly

From David Einhorn to Warren Buffett, their most important filings are now all in one place — simplified, visual, and always up-to-date.

Enjoy fishing for ideas!

Q4 2025 INVESTOR LETTER SUMMARIES

- Given the extreme level of current U.S. equity market concentration relative to recent history, one might assume this trend will eventually revert. However, it is helpful to consider what it would take for the weight of the ten largest companies in the S&P 500 to return to the pre-2020 average of 20.8%.

- In one such scenario, if the largest stocks were to remain flat, the rest of the index would need to return more than 160%. Given the scale required for full reversion, it seems likely that markets could remain highly concentrated for some time.

- Investors who believe concentration will persist may wish to consider its effect on their portfolio’s risk characteristics and alpha potential. They may also want to consider how those effects might be addressed most efficiently. This may include questioning managers’ risk models, expanding the opportunity set by allowing short positions, or re-evaluating the level of tracking error that best aligns with manager skill and portfolio objectives.

- First, I offer profound apologies to Joni and to her dark yacht-rock devotees under the sun, wherever they may sail. From the quote above, I have a guess about what they might think about artificial intelligence.

- Warren will stay on as chairman indefinitely, and he will be in the office daily. Slowing down at 95, particularly with reading, stepping away from day-to-day responsibilities must be bittersweet. I am sure Warren always believed he would go out in the proverbial pine box, just as Charlie did at age 99 in late November 2023, only 34 days shy of his 100th birthday.

- The active, value-oriented investor should have prospective advantages over the broad stock market at secular peaks and secular plateaus. That investor should also have advantages against capitalization-weighted stock indices trading at lofty valuations. The bursting of the late 1990s dot-com and communications bubble proved a terrific time to launch Semper Augustus.

- Over the last few weeks, we have seen a resurgence in market volatility that has been driven by the “AI Scare Trade.” Like a virus, it started with software, then spread to internet companies, and then broadened further into sectors like insurance, financial services, and real estate services. Anything that is asset-light and operates primarily in the digital world is facing the market’s wrath.

- After three years, the AI cycle is shifting from building core infrastructure to attacking real-world applications. Investors are in a fog of war as they try to figure out what that means for incumbent companies. They are asking which legacy firms will be beneficiaries and which are prone to disruption.

- What is unusual about the current drawdown is that many software companies, which have borne the brunt of the sell-off, are still growing. For example, ServiceNow just reported 21% year-over-year growth, and Atlassian reported 23% year-over-year growth. We have not yet seen evidence of AI materially affecting these businesses.

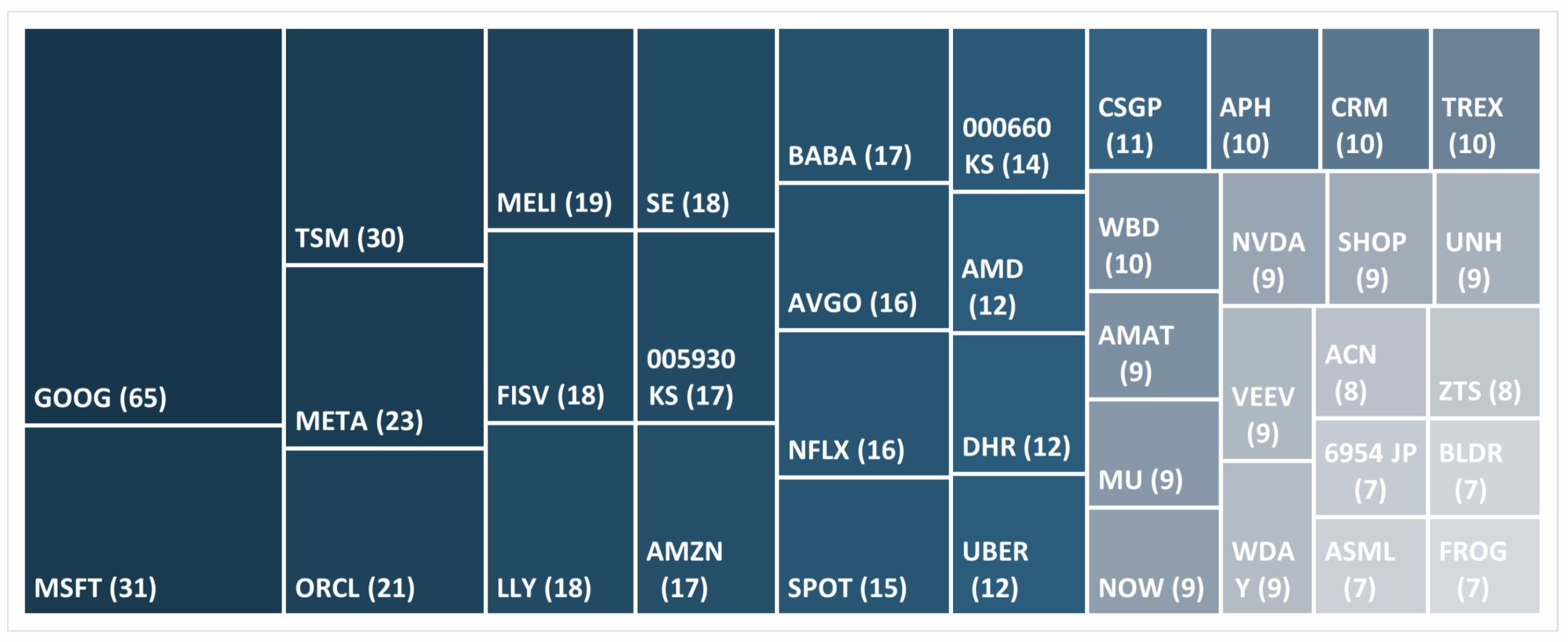

Q4 2025 TICKER TREEMAP

This quarter’s treemap of mentioned tickers (by Count)

ELEVATOR PITCHES BY FUNDS

Tamarack Valley Energy (by Barometer Capital)

- Tamarack Valley has designed a scaled 2026 capital program of approximately $400 million, specifically aimed at maximizing total returns while maintaining flexibility in a fluctuating commodity price cycle.

- The company’s “Clearwater” asset remains the primary engine of growth, with over 70% of the budget dedicated to primary development and waterflood expansion to mitigate decline rates.

- At a budget assumption of $60 WTI, Tamarack is projected to generate significant free funds flow while delivering strong shareholder returns through base dividends and share buybacks.

IHS Holding Ltd. (by City Different Investments)

- IHS Holding is currently at the center of a landmark $6.2 billion merger agreement with MTN Group, announced on February 17, 2026. Under the terms of the deal, shareholders will receive $8.50 per share in cash, representing a significant premium over recent trading levels.

- While our exposure to emerging markets will always be limited, we see attractive potential in this recovery story—in an industry we have known for years. IHS is the 5th largest independent tower company in the world, operating approximately 37,000 towers across seven countries in Africa and Latin America.

- For details, please see our recent synopsis, IHS Towers: A Comeback Story for 2026.

![]()

Occidental Petroleum Corp (by Mott Capital)

- Both Occidental and the energy sector haven’t performed this poorly versus the S&P 500 since the dot-com bubble. Additionally, oil appears to be the only commodity that is not performing well.

- Occidental seemed like a good way to play a rise in oil prices, given its tight relationship with the commodity. Additionally, it has a strong shareholder base, with Berkshire Hathaway owning more than 26% of the stock.

On top of that, the five largest shareholders own a combined 51.6% of the shares, which means that most of the shares are “locked up,” and if buyers step into the name, there will be fewer shares available to buy, potentially adding to an advance.

HIGHLIGHT OF THIS WEEK

MEDIA APPEARANCES BY BSDs

Boaz Weinstein Is Hunting Blue Owl’s Funds

-

-

-

-

-

- Boaz Weinstein’s investment firm Saba Capital and Cox Capital are preparing a tender offer for stakes in three semi-liquid private-credit funds operated by Blue Owl Capital.

- Saba and Cox announced Friday plans for a buyout offer to shareholders at prices between 65% and 80% of net asset value, an apparent effort to capitalize on rising angst about funds Blue Owl and other private fund managers marketed to individual investors.

-

-

-

-

-

-

-

-

-

- David Tepper, billionaire founder of hedge fund Appaloosa Management, sent a strongly worded letter to Whirlpool’s board, accusing the appliance maker of destroying shareholder value and calling for sweeping changes to its strategy.

- Tepper said in the letter that he watched with “a certain astonishment” as the company issued equity in what he called a large and unnecessary dilution of shareholders.

-

-

-

-

-

-

-

-

-

- Ken Fisher, founder, Executive Chairman and Co-Chief Investment Officer of Fisher Investments, addresses two pressing questions: Do recent layoffs and unemployment data signal a recession, and will AI permanently replace many jobs?

-

-

-

-