Happy Friday!

In this week’s letters,

– Saltlight Capital on AI Capex;

– African Lions Fund on African Frontier Equities;

– Cove Street Capital on the Bubble and Speculation;

– Elevator pitches for EXTR; SE; RELY

Quarter in progress: 794 fund letters of Q4 are live on our database!

We just launched the BSD 13Fs Investor Page, your new central hub to:

![]() Search BSD Gurus by name, portfolio value, or ticker

Search BSD Gurus by name, portfolio value, or ticker

![]() Track 13F filings from 100+ top hedge funds and BSDs

Track 13F filings from 100+ top hedge funds and BSDs

![]() Compare turnover rates, holdings, and portfolio shifts

Compare turnover rates, holdings, and portfolio shifts

![]() Spot new positions and high-conviction moves instantly

Spot new positions and high-conviction moves instantly

From David Einhorn to Warren Buffett, their most important filings are now all in one place — simplified, visual, and always up-to-date.

Enjoy fishing for ideas!

Q4 2025 INVESTOR LETTER SUMMARIES

- Entering 2026, the AI epoch remains transformational, and, as a theme, it has dominated US equity markets in both size and mindshare. The market, however, is struggling to price it coherently. We see three paradoxes today and, importantly, these interdependent observations cannot all be true at once.

- Upstream supply-chain participants are increasingly signalling that 2028 and beyond capex could be materially higher, not lower: This signal directly contradicts the widely held “digestion” narrative, which assumes that AI-driven capex will taper meaningfully over the medium to long term.

- Market scepticism toward NVIDIA analyst revenue forecasts: Sell-side analysts have increased their cumulative revenue projections for NVIDIA by $1.1 trillion over the next five fiscal years. However, the current share price suggests that the market harbours significant doubt about the achievability of these elevated expectations.

- AI ROI is unclear, yet software is being repriced as if disruption is certain: SaaS multiples have derated sharply on fears that AI will disintermediate seat-based software, even as many investors remain sceptical about near-term AI payback.

- My theory, though I’ll admit it’s unproven, is that if, as it appears, we are in a bull market for African frontier equities, liquidity should, all else equal, improve. There will be more buyers and sellers taking a closer interest in frontier African equities and putting more money to work.

- There has also been a proliferation of new investment fund products in Tanzania, spawning new demand for equities. What’s missing is IPOs. We are hopeful that, as the bull market gathers steam and valuations climb, some privately held businesses, or government-owned enterprises, may be attracted to list.

- The message, I think, is that, yes, definitely, everyone should be concerned about currency depreciation when investing in Frontier African markets. But these are not the only currencies where big depreciations can happen. Look at the yen. It’s lost a whopping 31.5%, or 6.9% per annum, in the time we’ve been running the Fund.

- Since no one really knows anything about the future, no matter how apparently dystopian, I don’t have to burden myself with any unease regarding my relative global standing in technology industry cognition.

- Do the words Pets.com bring anyone to January 2000? There were 14 AI Super Bowl commercials in 2026, which “rhymes” with what happened to the ad spenders from 2000, but there simply is not a “good enough” paper for me to confidently nod my head to with a smirk. And yes, there were actually Nobel prizes awarded to those who “proved” efficient markets.

- What most of 2026 has shown is how little money on the margin is “investing” and how much is “whatever” leveraged in large pods of capital with apparently tight stop-losses, where selling on the way down is the natural corollary to buying on the way up.

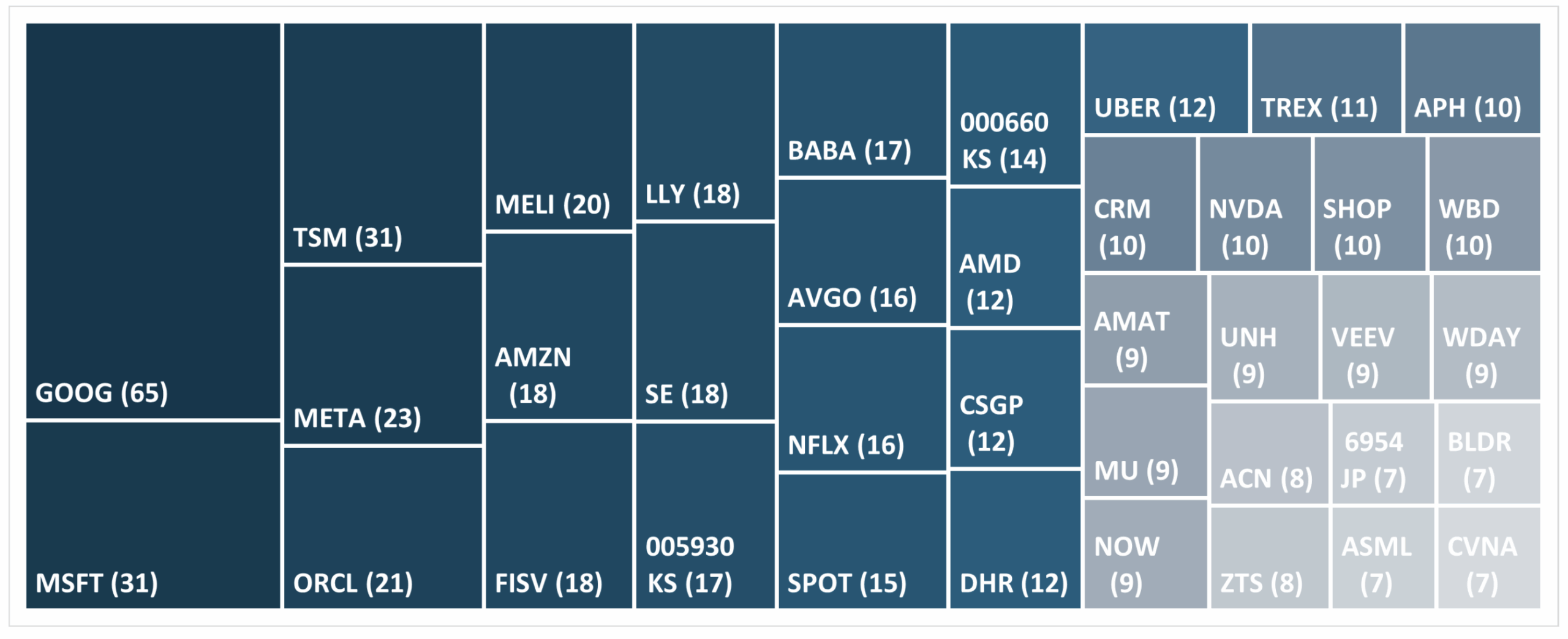

Q4 2025 TICKER TREEMAP

This quarter’s treemap of mentioned tickers (by Count)

ELEVATOR PITCHES BY FUNDS

![]()

Extreme Networks (by SouthernSun SMID)

- We believe EXTR has the opportunity to grow revenues in the low double-digit range and gain market share due to advantages in product architecture, pricing, and customer experience.

- Given Extreme Networks’ competitive positioning, improving mix of recurring revenues, and attractive valuation, we believe the company fits well within both of our strategies, where we seek businesses with strong market positions, financial flexibility, capable management teams and clear opportunities to improve operating performance and the potential to compound value over time.

![]()

Sea Limited (by Hayden Capital)

- Sea Limited shares have declined ~-45% over the past few months. The magnitude of the decline over the last few months is surprising, especially given that not much has changed in their fundamentals.

- The company’s e-commerce arm is projected to increase its Gross Merchandise Value by over 25% in 2026, fending off intense competition from TikTok Shop and Temu through aggressive logistics investments.

- So what’s priced in after the stock decline? At ~$107, Sea Limited is trading at roughly 7x 2028

EV/EBITDA, with +30% y/y EBITDA growth.

![]()

Remitly Global (by Unconventional Value)

- Remitly is capable of sustaining a mid-teens or higher growth rate while steadily expanding margins.

- Modest execution gives you a business earning well in excess of the current multiple, while the bear case means a structural break in a trend that has persisted for a decade. This is a company I suspect will improve over time, not deteriorate.

- The path to 20%-plus operating margins seems credible and not overly dependent on pricing power. A new customer typically generates gross profit in excess of the upfront cost in the first year and remains active for years, producing the 6x LTV/CAC the business has maintained to date.

HIGHLIGHT OF THIS WEEK

MEDIA APPEARANCES BY BSDs

-

-

-

-

-

- Legendary macro investor Stan Druckenmiller joins Hard Lessons for a conversation with Iliana Bouzali.

- Druckenmiller reflects on his early career and how he learned to act decisively and change course quickly when the facts on the ground shift. Hear how he would construct a portfolio if he had to start over today, why contrarianism is overrated, and which stock he regrets selling too early.

-

-

-

-

-

-

-

-

-

- There is a massive difference between taking a large initial position and allowing a position to become large. Few investors understand this distinction.

- Taking a large initial “at-cost” position is the investment equivalent of getting married after one date. In contrast, building conviction in a management team and business is like building trust in a relationship. It can’t be rushed. Trust is built at the beat of its own drum. Every position is unique, just like every relationship is unique, and conviction scales differently with each investment.

-

-

-

-

-

-

-

-

-

- John Arnold is a legendary energy trader and philanthropist. We cover what he learned from studying the unmatched scale and speed of China’s manufacturing base, the flywheel that gave him “the best seat in the industry” as a natural gas trader, and his systems-level tour of the challenges facing America’s energy, education and healthcare sectors.

-

-

-

-