Happy Friday!

In this week’s letters,

– Pernas Research on the mean reversion and market fundamentals;

– Pantera Capital on the bright side of crypto;

– Bridgewater Associates on the current market dynamics and the AI;

– Elevator pitches for HERDEZ MM; MSA; UTHR;

Quarter in progress: 460 fund letters of Q4 are live on our database!

Want to know what BSDs are buying (or selling)?

We just launched the BSD 13Fs Investor Page, your new central hub to:

![]() Search BSD Gurus by name, portfolio value, or ticker

Search BSD Gurus by name, portfolio value, or ticker

![]() Track 13F filings from 100+ top hedge funds and BSDs

Track 13F filings from 100+ top hedge funds and BSDs

![]() Compare turnover rates, holdings, and portfolio shifts

Compare turnover rates, holdings, and portfolio shifts

![]() Spot new positions and high-conviction moves instantly

Spot new positions and high-conviction moves instantly

From David Einhorn to Warren Buffett, their most important filings are now all in one place — simplified, visual, and always up-to-date.

Enjoy fishing for ideas!

Q4 2025 INVESTOR LETTER SUMMARIES

- Our conclusion is that today’s economy is fundamentally different, and that frequentist approaches that derive heuristics from historical data and apply them mechanically in order to gain insight into the future are increasingly flawed.

- What is true at the macro level is also true at the micro level. Investment philosophies that lean on mean reversion are particularly susceptible to severe underperformance. Mean reversion can be thought of as a form of reverse extrapolation: instead of assuming that current trends will continue, it assumes the opposite—that poor performance is likely to reverse simply because it has deviated far enough from the norm.

- This also implies that investor education itself has to evolve. Frameworks like Michael Porter’s Five Forces train analysts to study competition within a fixed industry boundary, implicitly assuming that the industry is the correct unit of analysis.

- First, institutional adoption continues to broaden. Enterprises are increasingly integrating blockchain into core products, ranging from Robinhood’s launch of tokenized equities to Stripe’s development of stablecoin infrastructure and JPMorgan’s tokenization of deposits.

- Second, product-market fit is becoming clearer. Stablecoins and prediction markets gained breakout attention and adoption as standout use cases in 2025, while broader tokenization and perpetual futures are showing early signs of product-market fit.

- Third, the macro backdrop is supportive. The U.S. economy remains resilient, with wage growth outpacing inflation and corporate earnings expanding. Liquidity conditions are improving now that the Fed has stopped quantitative tightening.

- Finally, penetration remains remarkably low. As Tom Lee of Bitmine has stated, there are just 4.4 million Bitcoin addresses holding more than $10,000 in value, compared with 900 million traditional investment accounts globally.

- Looking into 2026, one of the dynamics that seems most underpriced to us is the effect of the AI capex boom on macroeconomic conditions. Much has been said about the particular companies undertaking AI capex and their earnings potential, but when we aggregate across companies to estimate the second-order, economy-wide effects, we arrive at impacts that appear much larger than consensus growth forecasts.

- Demand for compute is rising exponentially as more consumers and businesses adopt AI and as companies race to train the next generation of models. The leading companies are now locked in a competitive resource-grab dynamic, committing to multiyear investment plans in order to secure necessary but scarce components.

- We are more confident about the impact of the AI capex boom on specific prices than we are about its overall impact on inflation because it will have mixed effects on the labor market and wages. On its own, AI capex is unlikely to be very labor-intensive, since most of the cost is equipment-related—chips, cooling equipment, and similar inputs—and once a data center is built, it requires very few people to operate.

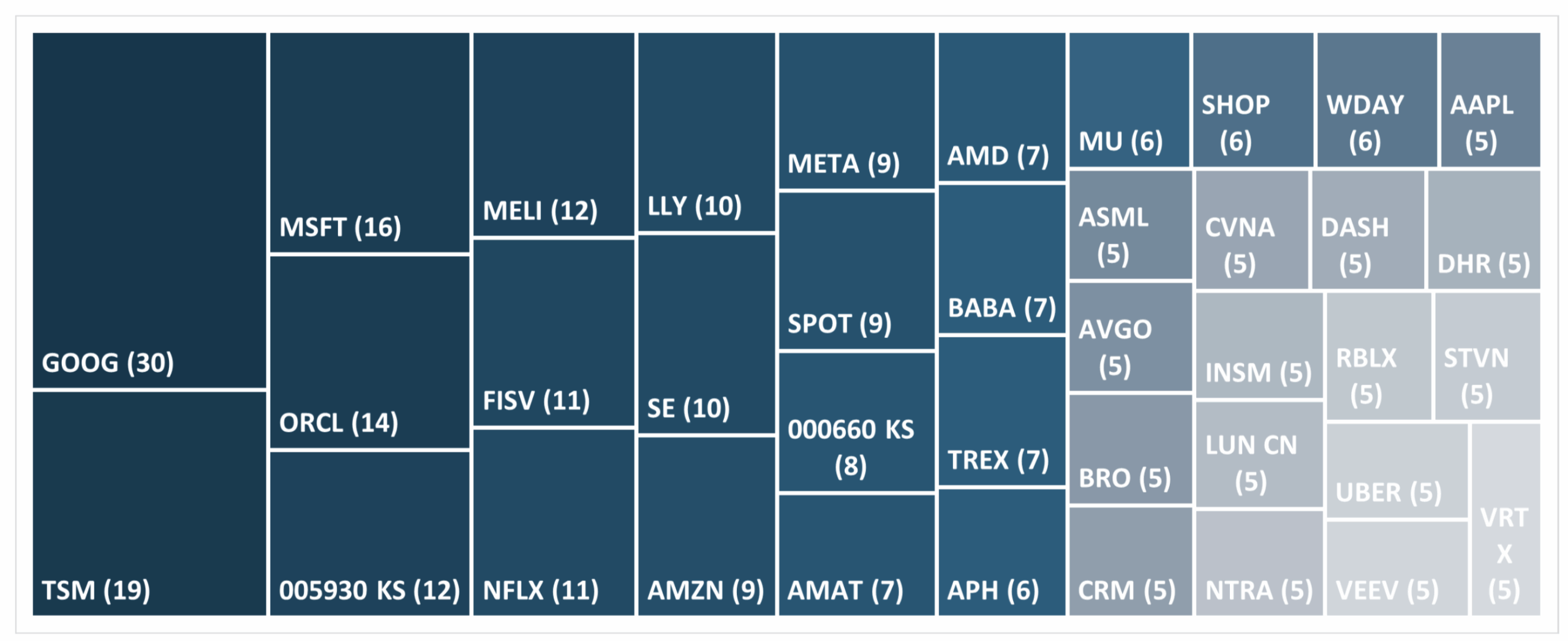

Q4 2025 TICKER TREEMAP

This quarter’s treemap of mentioned tickers (by Count)

ELEVATOR PITCHES BY FUNDS

![]()

Grupo Herdez (by Harding Loevner)

- Within Consumer Staples, Grupo Herdez, Mexico’s leading packaged-food manufacturer, posted solid results and completed two transactions that helped streamline its business.

- It sold a stake in a joint venture with US spice giant McCormick to its partner, with the proceeds potentially going toward stock buybacks. It also spun off its lower-returning Grupo Nutrisa business of coffee shops and yogurt stores.

- Distribution reach is a real moat in Mexico’s fragmented retail market. Capital allocation has been conservative, favoring stability over splashy growth. This is not a high-growth consumer name. It’s a survival-first compounder.

MSA Safety (by Madison Mid Cap Fund)

- MSA Safety sells protection equipment where compliance and reliability matter more than price. Regulatory standards and safety requirements create enduring demand. Customers don’t switch suppliers lightly when lives and liability are involved. Growth is steady, not flashy, but visibility is strong.

- Investors overlook safety equipment as niche industrial. Yet industrial incidents, regulation, and automation all increase demand. Margins benefit from brand trust and certification barriers. Recurring replacement cycles add stability. This is safety infrastructure that compounds quietly over time.

![]()

United Therapeutics Corp. (by Polaris Global)

- United Therapeutics is a biotech that behaves like an industrial company, which is exactly why it works. Its pulmonary hypertension franchise throws off enormous, durable cash flow.

- Pipeline investments are self-funded, not dependent on capital markets. Investors worry about concentration risk, but lifecycle extensions and new indications mitigate it. Management prioritizes capital returns alongside R&D, a rare combination in biotech.

- The organ manufacturing ambition adds long-dated optionality without pressuring the core business. Execution has been consistently conservative and effective. This is biotech without existential drama. Cash flow buys patience.

HIGHLIGHT OF THIS WEEK

MEDIA APPEARANCES BY BSDs

-

-

-

-

-

- A lot of people get rich, uh, in the stock market for the time being. Doesn’t change the laws of nature. The higher the market, the lower the returns will be.

- The only thing that you found that really works is is value… And that’s quality. A AAA bond yields a point less than you tell a B bond, let’s say. And everyone thinks that’s right and proper. You you buy a high quality bond, you take less risk, you should make less return. But the AAA stocks do not.

- Every bubble has always broken… if you look at that housing bubble, it is perfect. Three years up, three years down. It looks like that. How is it possible for the Fed boss with his statisticians, his advisers right at the peak of a three sigma outlier to say that the business is normal?

-

-

-

-

-

-

-

-

-

- I think the president has an extraordinary instinct. For the problems that both the United States and the free world face. I often don’t agree with his solutions, but I admire his ability and his willingness to forcefully talk about the problems that we face both in the United States and in the free world.

- Well, I actually think there’s a there’s an explicit warning that if your fiscal house is not in order, the bond vigilantes can come out and extract their price.

-

-

-

-

-

-

-

-

-

- On the other side of trade deficits and trade wars, there are capital and capital wars. If you take the conflicts, you can’t ignore the possibility of the capital wars. In other words, maybe there’s not the same inclination to buy at U.S. debt and so on.

- We know that both the holders of U.S. dollars are denominated … and those who need it, the United States, are worried about each other. Right? So if you have other countries that are holding it, and they’re worried about each other, and we’re producing a lot of it, that’s a big issue.

-

-

-

-