Happy Friday!

In this week’s letters,

– Baumann Capital on market valuation and investor conviction;

– Staude Capital on tariffs and inflation;

– RGA Investment Advisors on AI and LLM;

– Elevator pitches for OSK; FSF NZ; JBSS

Quarter in progress: 813 fund letters of Q4 are live on our database!

We just launched the BSD 13Fs Investor Page, your new central hub to:

![]() Search BSD Gurus by name, portfolio value, or ticker

Search BSD Gurus by name, portfolio value, or ticker

![]() Track 13F filings from 100+ top hedge funds and BSDs

Track 13F filings from 100+ top hedge funds and BSDs

![]() Compare turnover rates, holdings, and portfolio shifts

Compare turnover rates, holdings, and portfolio shifts

![]() Spot new positions and high-conviction moves instantly

Spot new positions and high-conviction moves instantly

From David Einhorn to Warren Buffett, their most important filings are now all in one place — simplified, visual, and always up-to-date.

Enjoy fishing for ideas!

Q4 2025 INVESTOR LETTER SUMMARIES

- Buying the same stocks is easy. The hard part is knowing what to do when they fall, when they rise, or when nothing happens for a long time. A stock that has gone up substantially may actually be cheaper than it was before. Two investors may own the same five stocks and still experience very different outcomes. The point is that it has always been public knowledge that Buffett owned Coke, yet very few investors had the conviction, and therefore the patience, to stay with the compounding for 38 years and earn a 30x return.

- Investors love simple numbers. Paying 10x earnings is considered cheap, while paying 30x is considered expensive. Unfortunately, investing does not work that statically. If it did, arbitrage would eliminate those opportunities almost immediately. In other words, you cannot go around claiming that low multiples are always good investments and high multiples are always bad ones.

- To properly value reinvesting compounders, you have to separate growth investments from the underlying earnings power of the business. If you add back the capital spent on opening new auto parts stores, the picture changes quickly. A business that initially appears cash-poor may actually be capable of generating substantial cash. That is the idea behind thinking through owners’ earnings.

- It is one of the most maddening conundrums in finance. We know that high market valuations are very good at predicting poor long-run investment returns, yet over the short run the predictive power of an overvalued market is essentially zero. Put more simply, just because something has gone up a lot recently does not mean it will stop going up tomorrow, even if we expect gravity to reassert itself eventually.

- If an honest assessment of the impact of Trump’s tariffs points to a longer-term headwind for the US economy, the second big-picture point that deserves more attention today is more optimistic. If you tune out the noise and look at the data, you see a US economy that remains in tremendous health.

- More important than their impact on inflation, however, is the position the US will find itself in if these early studies accurately describe the effect tariffs will have over time. In that case, the negotiating position of the US is much weaker than Trump likes to suggest, especially against other developed countries.

- One limitation we are highly aware of is that most AI systems are optimized for “agreeableness” rather than adversarial critique. In many of our use cases, we want the opposite. We use AI to challenge our assumptions and surface flaws in our reasoning.

- LLMs are phenomenal for saving time and streamlining processes. They have been incredibly helpful in getting to “no” faster on ideas and have accelerated our ability to turn over more rocks. That does not mean we do less work. On the contrary, it allows us to do more work and analyze even more companies in the search for ideas that truly fit our process.

- One of the simplest angles to consider in software came from our own experiments with vibe-coding tools, meaning AI-assisted code development, at RGA. Some mornings we wake up and, for whatever reason, one of the tools we built no longer works.

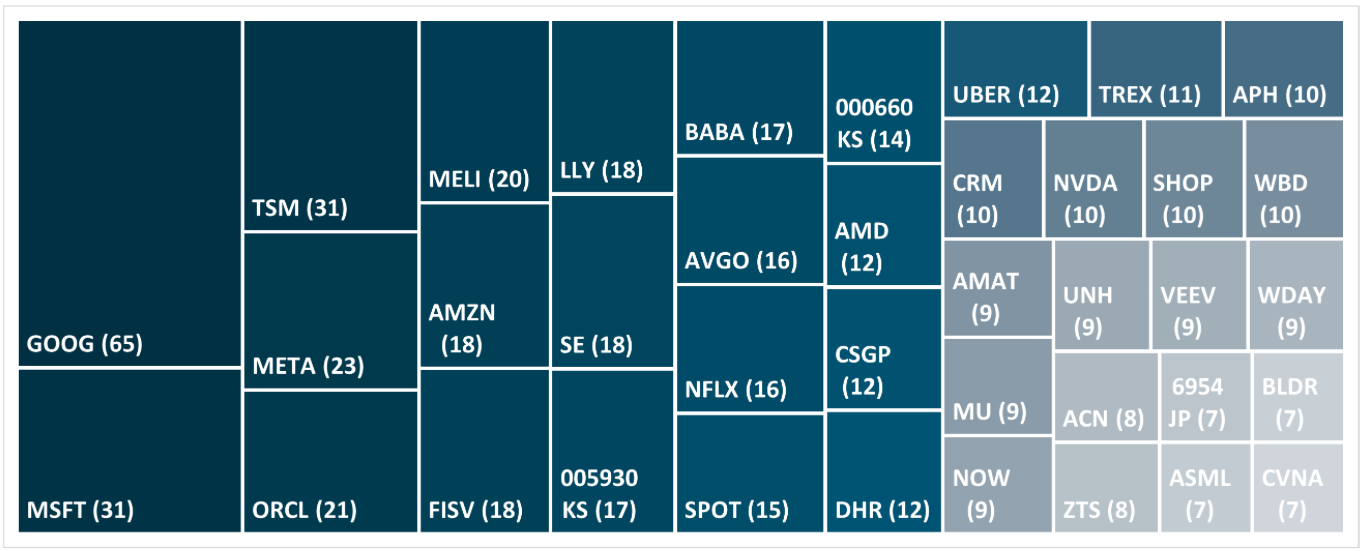

Q4 2025 TICKER TREEMAP

This quarter’s treemap of mentioned tickers (by Count)

ELEVATOR PITCHES BY FUNDS

![]()

Oshkosh Corp (by SouthernSun SMID Cap)

- OSK is a global manufacturer of specialized vehicles and equipment used in essential and mission-critical applications.

- Oshkosh also holds strong positions in airport equipment, including aircraft rescue and firefighting vehicles, ground support equipment, and passenger boarding bridges, where safety, reliability, and long service life are critical and competition is limited.

- Supported by a strong backlog, a solid balance sheet, and shares trading at a discount to long-term earnings potential, we believe Oshkosh is well positioned to deliver improving profitability and shareholder value over time.

![]()

Fonterra Shareholders Fund (by Tactile Fund)

- Much of the milk produced by these cows and many more just like them is processed by Fonterra Co-operative Group Limited, the largest dairy co-op in the country.

- Fonterra, in which Tactile Fund holds an economic interest through Fonterra Shareholders Fund, has 24 domestic manufacturing sites, including a facility nearby in Eltham—just on the other side of Mount Taranaki.

- Fonterra struck an agreement to sell its consumer-facing businesses to dairy powerhouse Lactalis.

- Looking long-term, I expect agricultural companies with strong geographic and/or cost advantages to be attractive performers.

John B. Sanfilippo & Son (by Cullen Small Cap)

- JBSS is a leading processor and distributor of tree nuts and peanuts, supplying branded, private-label, and ingredient products across retail, foodservice, and industrial end markets.

- The company benefits from structurally stable demand driven by long-term health and protein consumption trends, with nuts increasingly positioned as a core pantry and snacking category.

- With durable cash flows, limited secular risk, and attractive valuation relative to earnings power, JBSS offers a compelling risk-adjusted opportunity within the consumer staples universe.

HIGHLIGHT OF THIS WEEK

MEDIA APPEARANCES BY BSDs

-

-

-

-

-

- I think one of the reasons we’ve rarely ended up in the semis is that we’ve found it really hard to get comfortable with the level of earnings that we feel highly confident is going to be achieved on average over the next five or seven years.

- We prize accuracy in forecast, not conservatism.

- We don’t focus on tracking error as our primary risk. We focus on drawdown risk as the risk we’re trying to mitigate.

-

-

-

-

-

-

-

-

-

- If we don’t see the progress, then we won’t see the rate cut.’ … If we don’t see inflation progress, we won’t see the rate cut. Well, right now our inflation model says that we’re headed to three and a half inflation rate for basically the second half of 2026. So that could not possibly be classified as progress on inflation. It’s anti‑progress on inflation.

- There was a very major private credit fund by an extremely well‑respected sponsor that in one day marked its fund down, a private credit fund, down 19% in a day.

-

-

-

-

-

-

-

-

-

- Burry, the former hedge fund investor famous for predicting and profiting from the subprime mortgage crisis, argues President Donald Trump’s handling of the conflict in Iran — including reports that Trump was considering “winding down” the war — is being shaped by his allergy to market dips.

-

-

-

-