Happy Friday!

In this week’s letters,

– Hinde Group on AI and economic expansions;

– Palm Harbour Capital on AI Bears & Bulls;

– Summers Value Fund on the healthcare sector and its recent dynamics;

– Elevator pitches for DG FP; FTAI; COF;

Quarter in progress: 629 fund letters of Q3 are live on our database!

Want to know what BSDs are buying (or selling)?

We just launched the BSD 13Fs Investor Page, your new central hub to:

![]() Search BSD Gurus by name, portfolio value, or ticker

Search BSD Gurus by name, portfolio value, or ticker

![]() Track 13F filings from 100+ top hedge funds and BSDs

Track 13F filings from 100+ top hedge funds and BSDs

![]() Compare turnover rates, holdings, and portfolio shifts

Compare turnover rates, holdings, and portfolio shifts

![]() Spot new positions and high-conviction moves instantly

Spot new positions and high-conviction moves instantly

From David Einhorn to Warren Buffett, their most important filings are now all in one place — simplified, visual, and always up-to-date.

Enjoy fishing for ideas!

Q3 2025 INVESTOR LETTER SUMMARIES

- The generative AI investment boom is one of the main factors keeping the economy afloat and the stock market ebullient amid the current political and economic turmoil. A handful of big tech companies, such as Google, Microsoft, Amazon, and Meta, have been steadily and dramatically ramping up their investments in large-scale AI data centers over the past several years to support the development and deployment of increasingly capable generative AI models.

- Although an economic expansion driven by massive, concentrated investments in a nascent technology would seem to be fragile, financial markets ended the third quarter pricing in an unusually low chance of things going sideways. Investment-grade and high-yield credit spreads ended the quarter, scraping their all-time lows.

- Markets expect the Fed to cut the federal funds rate several times by the end of next year, but assign a low probability to the benchmark rate falling much below a level that the Fed considers neutral over the long term.

- Recent commentary has started to ask whether we are in a bubble,or at least an AI bubble. We take no view on this, but we do think valuations, particularly in the US and India, are at nosebleed levels.

- Some argue that valuations are less relevant today, or that historical comparisons no longer apply. The prevailing view is that “this time is different”: companies are stronger, balance sheets carry less leverage, and profitability is robust. While we agree that today’s environment differs from the late-1990s technology bubble, we see certain parallels.

- Bulls contend that these are not profitless speculative ventures. Yet questions remain. OpenAI, for example, is loss-making and its revenue model remains unproven, even as it strikes multi-billion-dollar deals without clear funding sources. Nvidia, though highly profitable, has engaged in what some analysts describe as “circular ”transactions to sustain growth.

- The healthcare sector has experienced a year of challenges leading to underperformance versus the broader indexes. New leadership at the Food and Drug Administration (FDA) has introduced regulatory uncertainty across the sector.

- Budget pressure at federal agencies including the National Institutes of Health (NIH) and Centers for Disease Control and Prevention (CDC) has weighed on healthcare spending. Potential adjustments to Medicaid eligibility have stoked fears of reduced reimbursement on healthcare products and services.

- Lastly, the administration has proposed to curb drug pricing using a most favored nation approach. These crosscurrents have made the healthcare sector one of the most complex corners of the stock market to navigate, souring sentiment and leading many generalist investors to pull back.

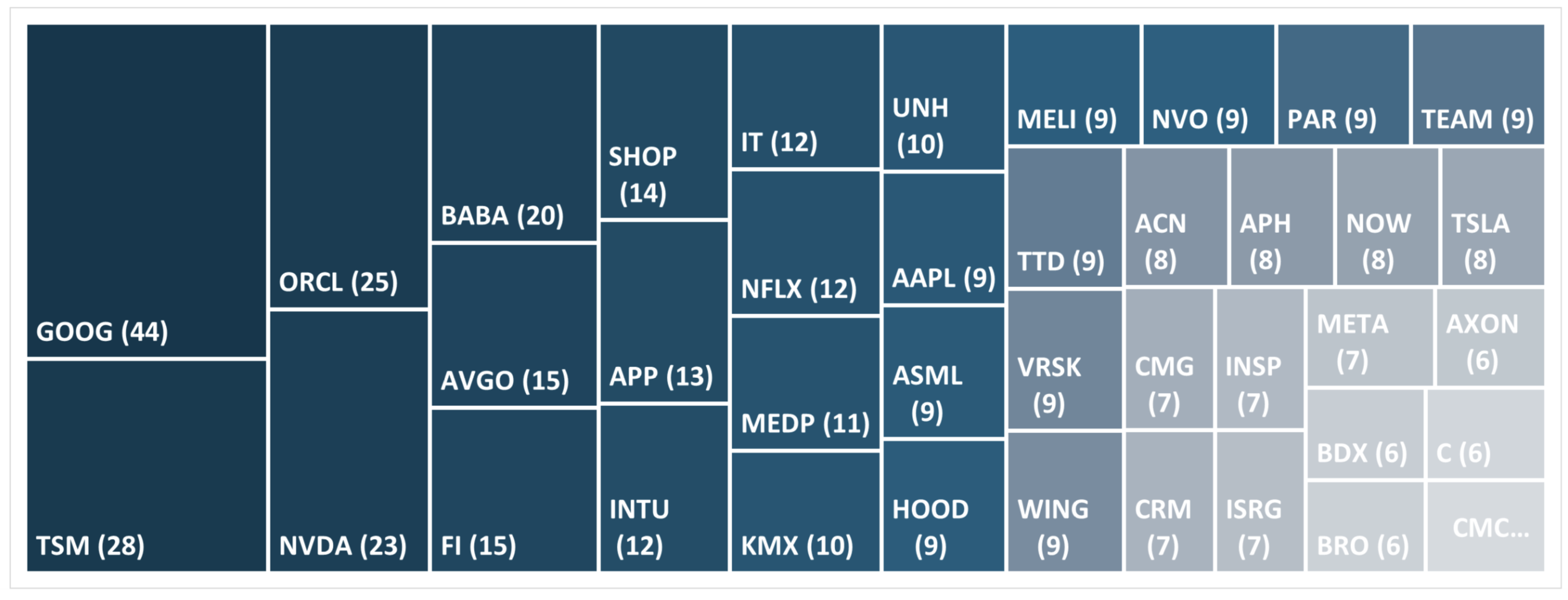

Q3 2025 TICKER TREEMAP

This quarter’s treemap of mentioned tickers (by Count)

ELEVATOR PITCHES BY FUNDS

![]()

Vinci SA (by Global High Dividend)

- Vinci is a major global operator of concessions and a provider of energy and construction services primarily in Europe.

- We believe that airports are an attractive long-term asset class given good prospects for passenger volume growth along with the ability to generate robust returns in non-regulated areas such as retail, food courts and parking lots.

- Vinci builds roads and civil engineers projects and buildings. While this division is not as profitable as the rest of the company, it provides Vinci with a competitive advantage in bidding for concession projects which often require some amount of construction.

FTAI Aviation (by Crossroads Capital)

- FTAI captures the most attractive economics in aftermarket aviation not by acting as a passive lessor but by operating as a vertically integrated industrial platform. FTAI utilizes its SCI, specifically through its maintenance centers, to manufacture ‘green time’ at a structurally lower cost relative to what the OEMs can provide.

- This creates a unique arbitrage in that FTAI’s customers can avoid downtime associated with “shop visits” thanks to its ability to provide immediate, highly visible part availability in a supply-constrained market.

- Ultimately, we believe that FTAI’s asset-light expansion and module production milestones position it as a top compounder in the aviation space for many years to come.

Capital One (by RGA Investment Advisors)

- The acquisition of DFS is a transformative transaction that uniquely positions COF to generate substantial value, fundamentally redefine its competitive standing, and reshape the US payments landscape.

- The most immediate and transformative value driver of the acquisition is the ownership of the Discover network, which allows COF to avoid regulatory constraints that cap interchange fees for most large banks.

- COF has historically made substantial investments in its tech stack, designed specifically to grow through acquisition and convert new portfolios efficiently onto its platform.

HIGHLIGHT OF THIS WEEK

MEDIA APPEARANCES BY BSDs

-

-

-

-

-

- Alan Howard, co-founder of Brevan Howard Asset Management, joined the ranks of wealthy individuals exiting the UK amid tax hikes, surfacing as a resident of Switzerland.

- The hedge fund founder relocated from Britain since early June to the Alpine nation, according to an analysis of UK registry filings by Bloomberg, which reported in 2024 that he was exploring the move.

- Howard’s departure signals growing unease among Britain’s home-grown talent as they grapple with higher taxes on everything from private equity investments to inheritances to capital gains under Keir Starmer’s Labour government.

-

-

-

-

-

-

-

-

-

- Paul Singer’s Elliott Investment Management Inc. convinced a judge to grant its request to liquidate an oil and gas fund as part of a legal fight with a Texas private equity firm managing the assets.

- Stronghold warned that any liquidation would hurt 100 other investors because it would have to sell assets at a discount to satisfy Elliott’s desire for short-term liquidity.

-

-

-

-

-

-

-

-

-

- “There is no doubt that the Western world needs Europe to be more successful” Citadel founder Ken Griffin said during in an interview at a conference in Paris Tuesday. Griffin spoke about the importance of a strong and prosperous Europe.

-

-

-

-