Happy Friday!

In this week’s letters,

– Robotti Value Investors on patience and contrarian investing;

– Praetorian Capital Management on potential asymmetric opportunities;

– Oaktree Capital Management on dispersion of financial assets;

– Elevator pitches for LIN; MCDIF; QURE;

Quarter in progress: 712 fund letters of Q4 are live on our database!

Want to know what BSDs are buying (or selling)?

We just launched the BSD 13Fs Investor Page, your new central hub to:

![]() Search BSD Gurus by name, portfolio value, or ticker

Search BSD Gurus by name, portfolio value, or ticker

![]() Track 13F filings from 100+ top hedge funds and BSDs

Track 13F filings from 100+ top hedge funds and BSDs

![]() Compare turnover rates, holdings, and portfolio shifts

Compare turnover rates, holdings, and portfolio shifts

![]() Spot new positions and high-conviction moves instantly

Spot new positions and high-conviction moves instantly

From David Einhorn to Warren Buffett, their most important filings are now all in one place — simplified, visual, and always up-to-date.

Enjoy fishing for ideas!

Q4 2025 INVESTOR LETTER SUMMARIES

- Over the years, we have often revisited an observation by German-born MIT economist Rudiger Dornbusch: “In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.” Our view has been different. We believe that recurring patterns trigger an economic response.

- Prolonged downturns force consolidation, and they often leave only a small number of well-capitalized operators standing. If these supply responses coincide with demand growth, the result can be a powerful secular shift.

- We have noted that the macro backdrop for an industrial renaissance in the Americas is being set by the vast availability of low-cost energy, particularly natural gas priced far below levels in the rest of the developed world. This pricing gap provides a persistent economic advantage and creates a strong incentive that acts as an enduring demand driver.

- In a world where we continue to inflate ever larger bubbles to bail out prior bubbles, there are only a limited number of sectors that merit focus while remaining disciplined as a value investor. That said, there are some compelling long-term trends, and I have doubled down on them over the past year.

- For more than a decade, emerging markets have been in a relative bear market as investor capital has migrated toward U.S. markets. As a result, many emerging markets have become quite inexpensive when viewed from a valuation perspective.

- Refiners have suffered for more than a decade, excluding the immediate aftermath of the war in Ukraine. During this period, many Western refiners chose to shut down rather than invest substantial capital in upgrades to meet questionable regulatory mandates. At the same time, China flooded global markets with refined products, undermining industry economics for nearly all participants.

- We believe we’re entering a new era in which the performance of financial assets is increasingly dispersed. Behind buoyant index averages, there are sharply bifurcated groups of winners and losers. Equities are flying high, but they are still being propelled mostly by a handful of AI superstars.

- U.S. economic data remains challenging to interpret, even though the headline metrics appear mostly positive. GDP growth has certainly surprised to the upside, with the economy recording a 4.4% annual growth rate in the third quarter of 2025. Resilient consumer spending has been a major contributor, but the picture behind the headlines is more complex.

- “Tight spreads but good yields” has become a familiar refrain in the sub-investment-grade credit universe. While that characterization is broadly accurate, a closer look under the hood reveals a more nuanced perspective.

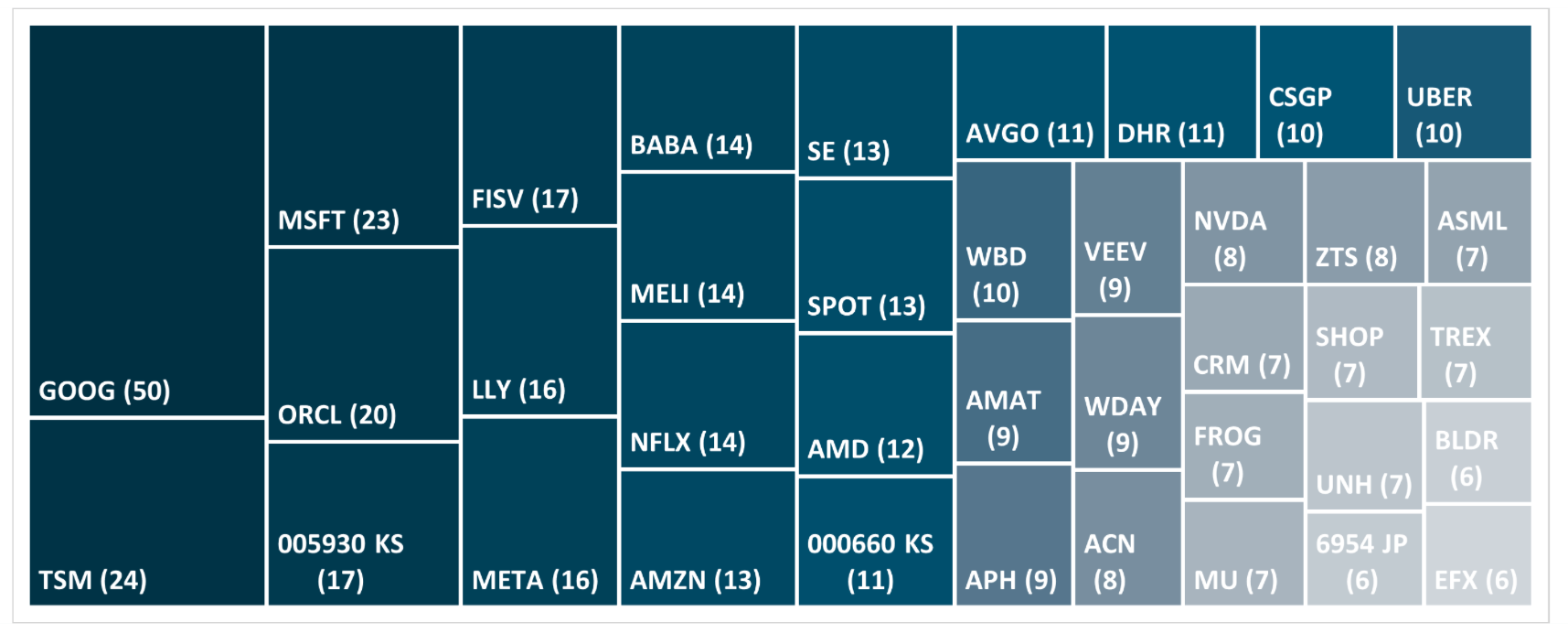

Q4 2025 TICKER TREEMAP

This quarter’s treemap of mentioned tickers (by Count)

ELEVATOR PITCHES BY FUNDS

![]()

- Linde is the largest industrial gas company in the world, operating in more than 80 countries.

- The industry benefits from powerful economies of scale, physics-driven efficiency advantages, and prohibitive transportation costs that require dense, localized distribution networks. Long-term take-or-pay contracts with cost pass-through provisions create inflation-protected, utility-like cash flows.

- Despite these strengths, Linde’s shares were pressured by a global industrial slowdown, which we believe caused investors to over-discount the business as near-term “dead money.”

![]()

McDermott Intl. (by Alluvial Capital Management)

- McDermott is now a core position for the fund. The company is working to refinance its debt, resume SEC reporting, and return its shares to a major exchange.

- Operating trends are improving, with 2025 adjusted EBITDA expected to exceed $400 million, up more than 70% year-over-year. McDermott has secured billions in new contracts for Middle Eastern national oil companies and energy transition projects.

- If execution continues and margins improve, I see upside to $60 or higher versus current trading in the mid-$20s.

![]()

uniQure N.V. (by Warden Capital)

- This is a biotech stock which has a potential groundbreaking gene therapy for Huntington’s disease called AMT-130.

- They presented their initial results back in September which showed disease progression slowing by ~75% 3 years after treatment, and the stock rocketed up to as high as $70/share. In a twist, the FDA came in 2 months later and rescinded their previous agreement to use an external matched control group to compare Qure’s treatment to, which has caused the stock to crash down to its current price of ~$23/share.

- Qure has a significant amount of cash on hand (~$700mm as of Q3, relative to its ~$200mm/year burn rate), and could fund a trial if they had to worst case.

HIGHLIGHT OF THIS WEEK

MEDIA APPEARANCES BY BSDs

-

-

-

-

-

- The branding of Kevin as someone who’s always hawkish is not correct. I’ve seen him go both ways.

- Warsh is “very open minded” to the monetary policy approach of former Fed chief Alan Greenspan, who oversaw the central bank in the 1990s during a period of intense productivity growth. Kevin right now very much believes you can have growth without inflation.

- I could not think of a single other individual on the planet better equipped.

-

-

-

-

-

-

-

-

-

- We used to buy all of a company, and I liked doing that as I don’t have to do a dance for a boardroom.

- Prices have become more reasonable, deals are becoming more productive. So we can do things the way we like to do them.

- I was hoping that the threat of tariffs was going to lower tariffs, so we had closer to free trade between us and our trading partners, and not being used as a source of revenue.

-

-

-

-

-

-

-

-

-

- Bitcoin, which is down 40% since its October peak, is now exposed as a completely speculative asset and does not qualify as a debasement hedge like gold or silver.

- If BTC prices fall further, it could significantly affect the balance sheets of major holders, trigger a sell-off across the crypto ecosystem, and ultimately lead to value destruction.

- There is no organic use case reason for Bitcoin to slow or stop its descent.

-

-

-

-