Happy Friday!

In this week's letters,

- Goehring & Rozencwajg Associates on oil, LNG and commodities;

- Headwaters Capital on the market concentration and small-caps;

- Giverny Capital Asset Management on the effects of AI;

- Elevator pitches for MELI; ORE CN; 4441 JP

Quarter in progress: 811 fund letters of Q4 are live on our database!

We just launched the BSD 13Fs Investor Page, your new central hub to:

Q4 2025 INVESTOR LETTER SUMMARIES

- The outbreak of hostilities in the Persian Gulf has already reverberated through global oil markets with remarkable speed. Rather than attempting a full survey of supply and demand trends in both oil and natural gas, which we will address in a future letter, we focus here on the more immediate consequences of the effective closure of the Strait of Hormuz.

- As of March 11, 2026, the Strait of Hormuz remains effectively closed, disrupting the transport of roughly 20 percent of global oil production and a similar share of seaborne LNG supply.

- China responded quickly on March 11 by imposing export restrictions on refined petroleum products in an effort to safeguard domestic supply. Meanwhile, rising U.S. shale production has sharply reduced American reliance on imported oil, leaving China as the world’s dominant crude importer by a wide margin.

- Recent price action has left the market as concentrated as it has ever been, and arguably even more concentrated than it appears, because the profits of many leading companies are tied to AI infrastructure spending. Valuation gaps between winners and losers have widened to historic extremes, while many high-quality businesses now trade at historically cheap multiples.

- In my view, today’s market offers as many opportunities and risks as I can remember. If you believe that earnings drive stock prices over the long term, then the trade in unprofitable companies should eventually reverse. It remains open to debate whether the AI trade will persist, but for now it largely represents a single bet on how much capital expenditure five companies will commit to building data centers.

- If you own the small-cap index, you are becoming increasingly exposed to both AI-related capital spending and unprofitable companies. In a historically concentrated market that is heavily levered to a single theme, I believe the value of an actively managed portfolio will become increasingly clear. That brings me to a business update for Headwaters Capital.

Giverny Capital Asset Management

![]()

- I believe that, over time, regardless of how artificial intelligence changes our lives, owning a portfolio of high-performing businesses should remain a satisfactory strategy. Our portfolio includes the country’s largest distributors of air conditioning and plumbing supplies, two of the most efficient insurance companies, a leading water treatment service business focused on small towns, and a highly profitable manufacturer of spare parts for airplanes, among others.

- AI is unlikely to displace these businesses. On the contrary, as skilled users of technology, they may improve efficiency and strengthen their competitive positions relative to smaller, subscale competitors through the adoption of AI tools.

- I am not smart enough to predict whether those returns will ultimately prove delightful or disappointing, much less to offer a confident view on whether we are in a bubble. However, any student of economic history knows that periods of rapid infrastructure buildout have often ended poorly for investors.

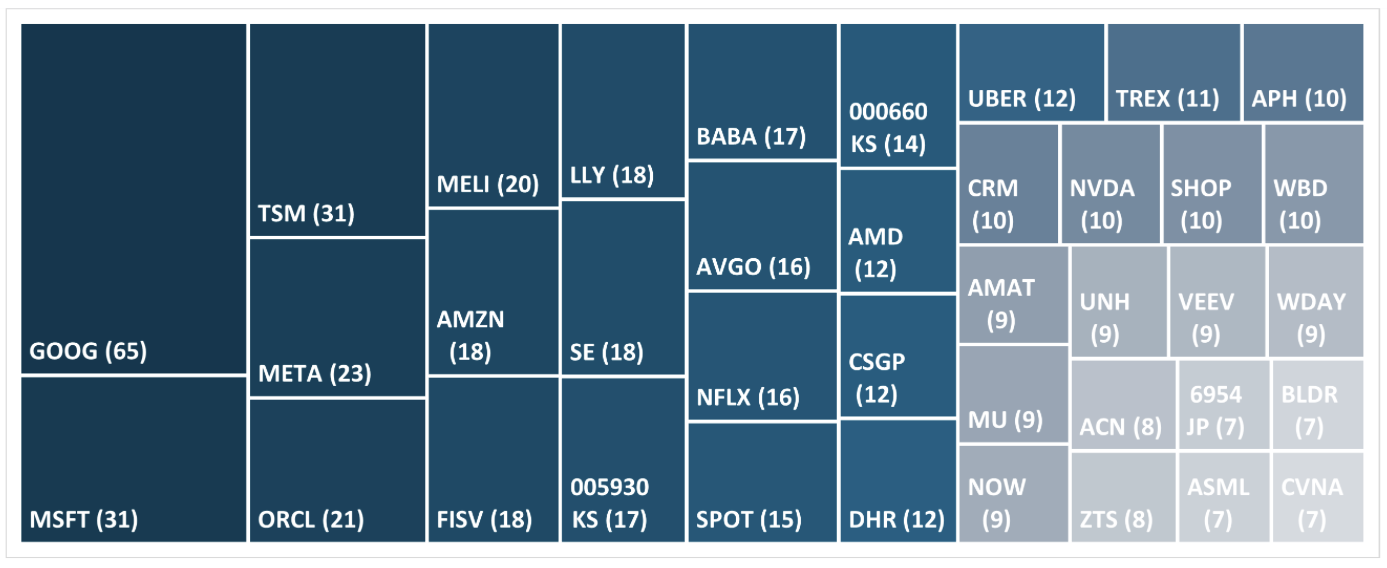

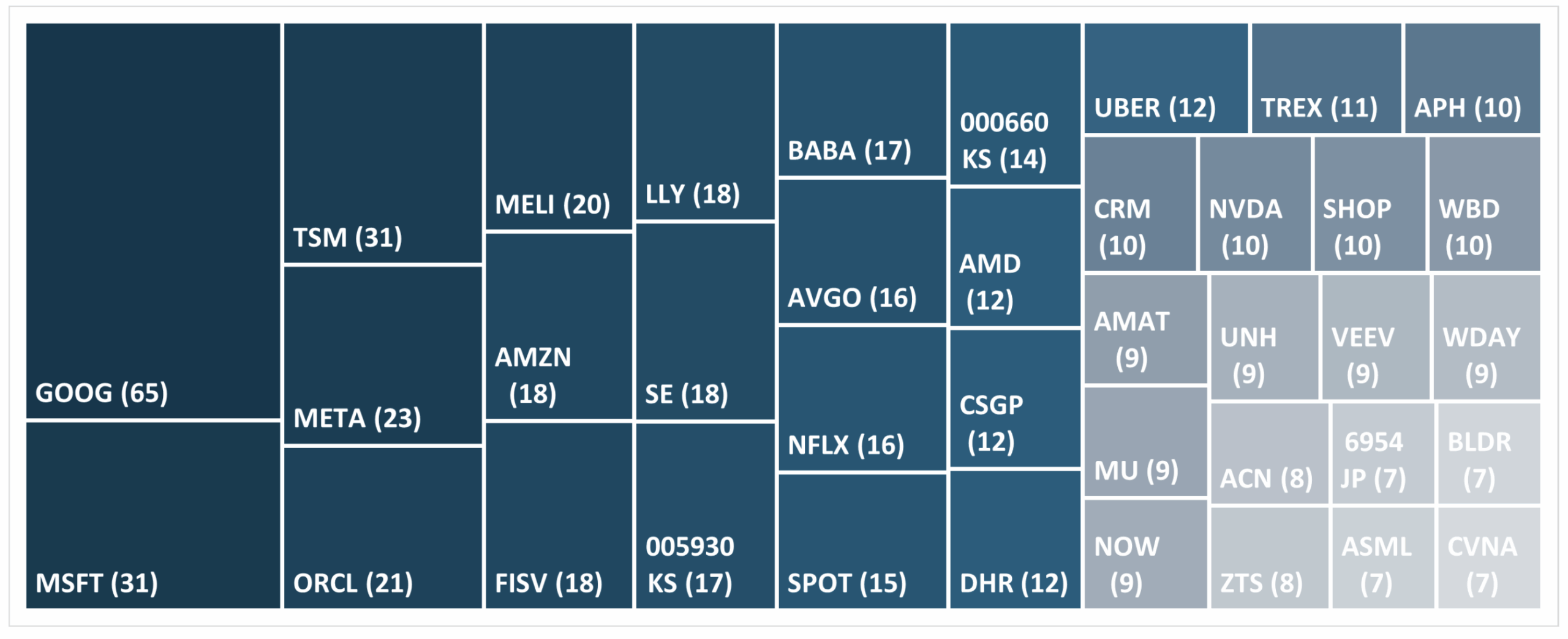

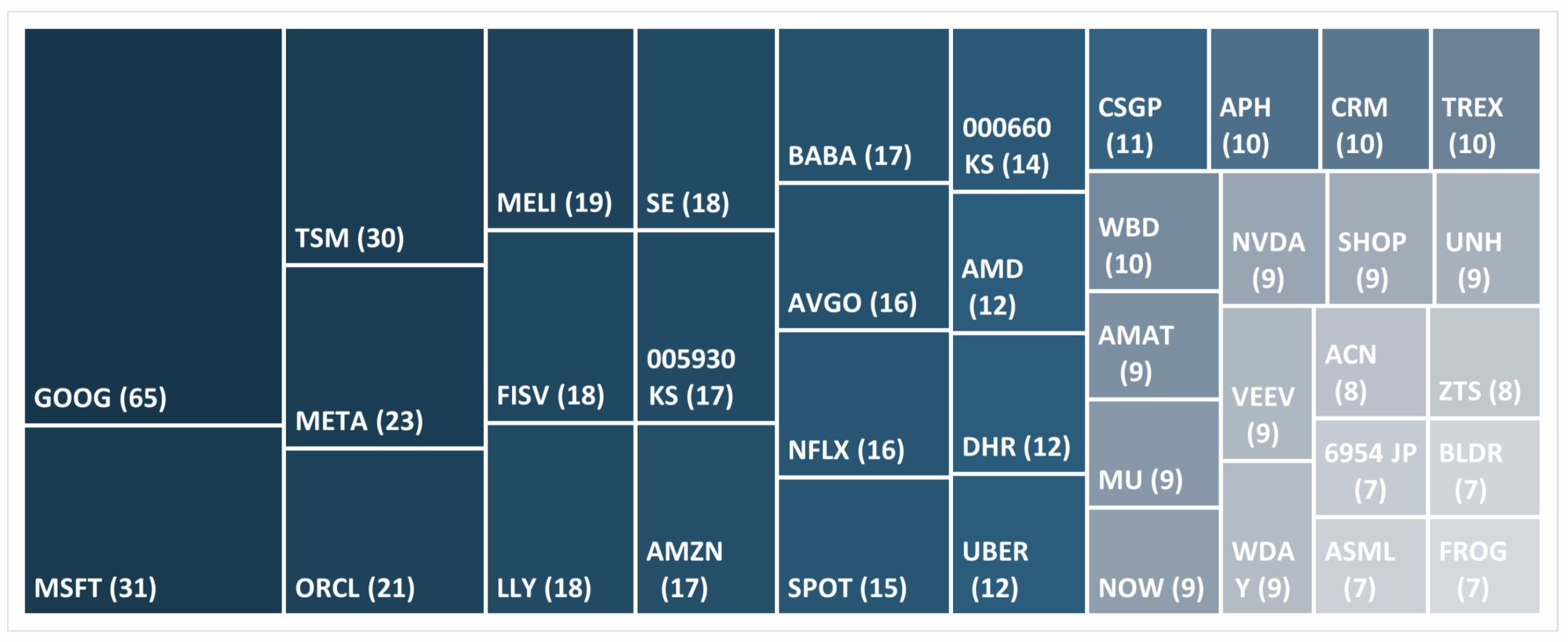

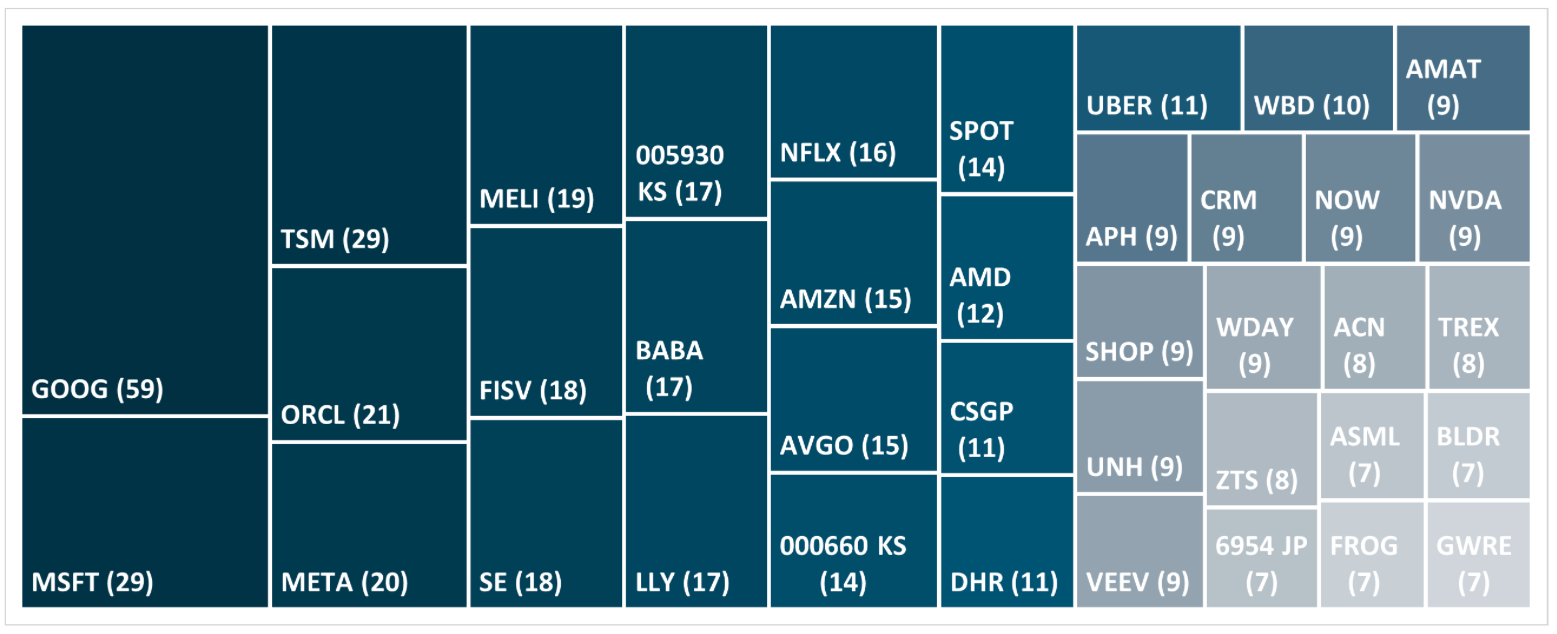

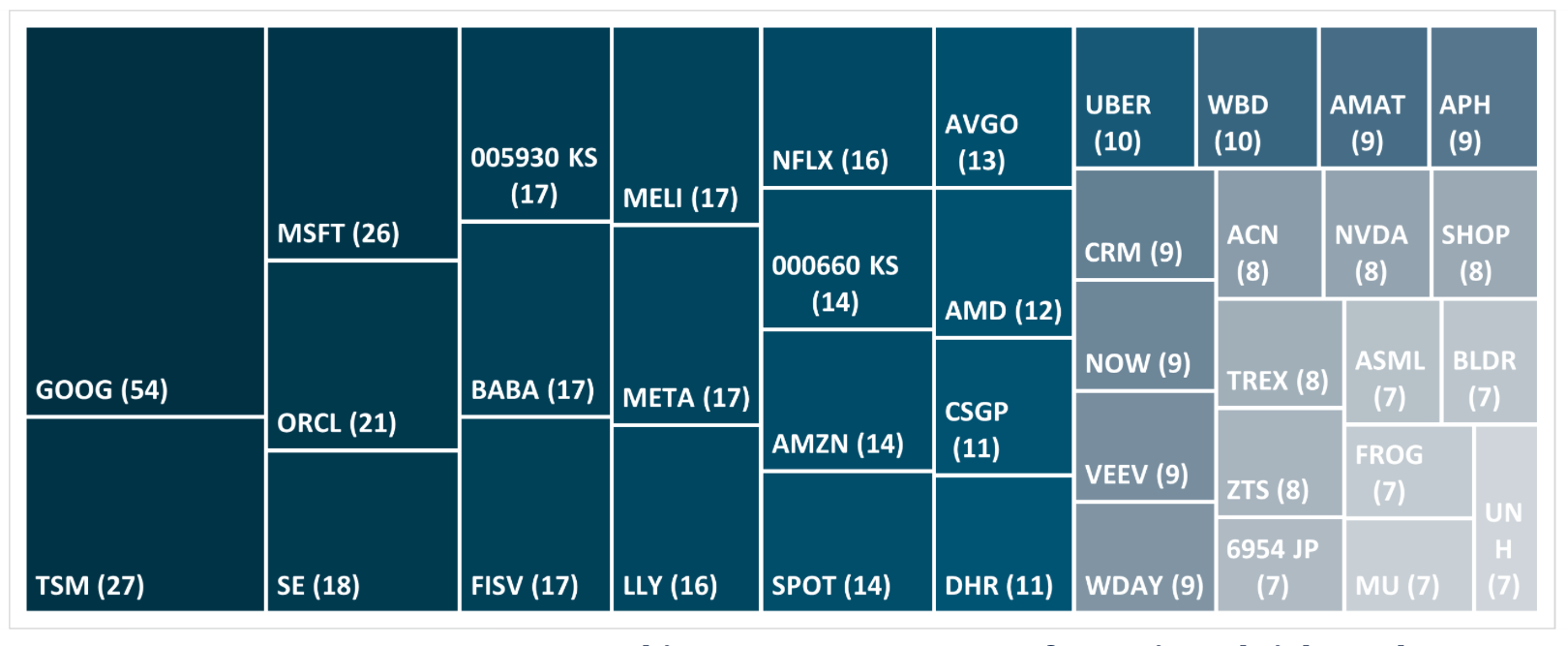

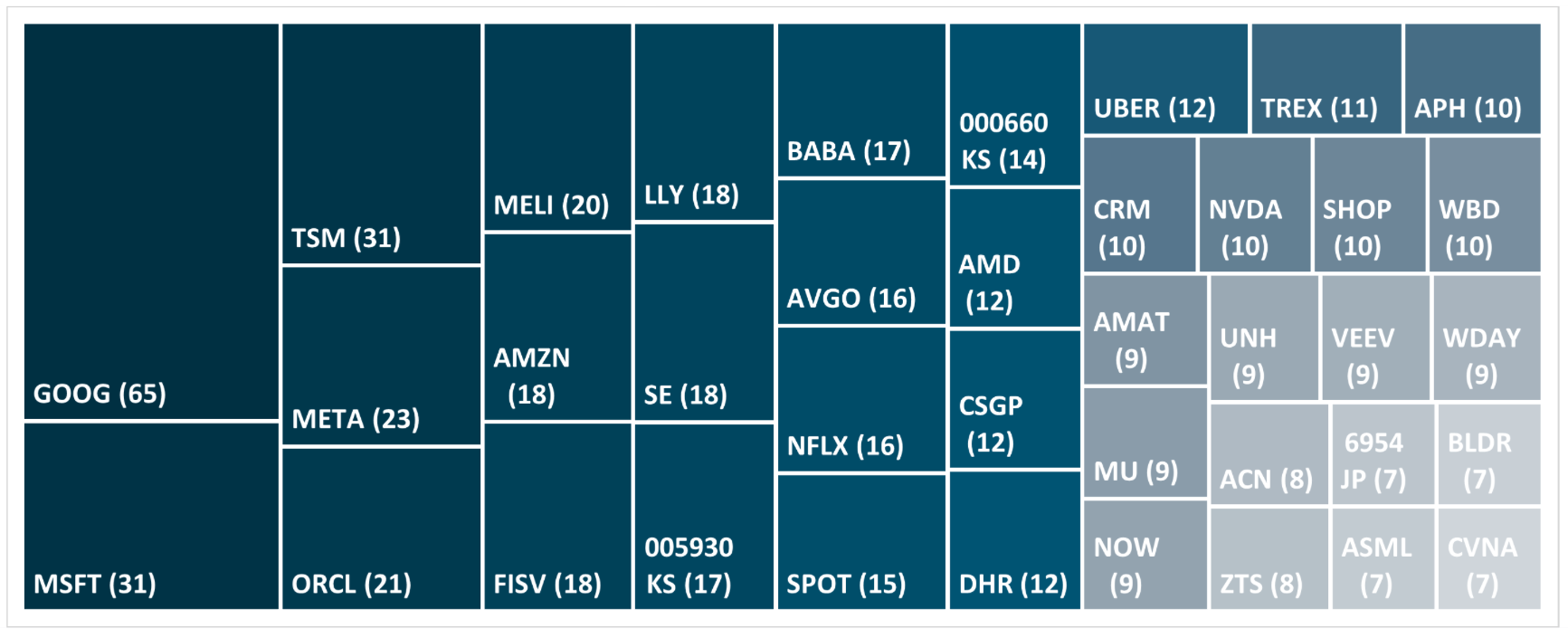

Q4 2025 TICKER TREEMAP

This quarter's treemap of mentioned tickers (by Count)

ELEVATOR PITCHES BY FUNDS

MercadoLibre (by Baron FinTech Fund)

- MercadoLibre, Inc., the leading e-commerce marketplace and fintech provider in Latin America, detracted from performance on concerns over competition and margin pressure.

- Continued volatility in Argentina, one of MercadoLibre’s fastest-growing markets, also raised concerns that weaker economic conditions could result in less reliable profit contribution.

- We maintain conviction in the company’s long-term opportunity. In our view, MercadoLibre is uniquely positioned to capture a significant share of Latin America’s underpenetrated e-commerce and fintech markets because of its scale, customer trust, and unique ecosystem.

Orezone Gold Corp (by Aegis Value Fund)

- Investor fears peaked when elements of the Burkina Faso government demanded partial divestment of a neighboring mine owned by West African Resources, leading to a halt in West African.

- Despite the country risk, Orezone continues its flagship Bomboré mine expansion project in Burkina, which is reported to be on track and should begin substantially improving production and cash flow from the mine in 2026.

- In January 2026, Orezone announced that it will acquire the Casa Berardi mine in Quebec from Hecla, adding a second mine in a much superior, top-tier jurisdiction.

Tobila Systems (by Smoak Capital)

- Tobila Systems is a Japanese company focused on fraud and spam call prevention. Tobila has successfully developed a new B2B growth engine that will accelerate revenue, profit, and free cash flow growth going forward yet amazingly trades at 4.5x EV/FCF with its B2B segment growing revenue over 50% per year.

- Tobila’s fast growing Solutions segment was effectively hidden from investors until last year when the company began to separately disclose TobilaPhone Biz and Cloud.

- Shares trade at only 4.4x EV/FCF and likely only 3x on an EV/Fwd FCF basis. Even at a low absolute multiple of 10-12x FCF, upside is 80-110%, and 140-180% on a forward basis.

HIGHLIGHT OF THIS WEEK

MEDIA APPEARANCES BY BSDs

-

-

-

-

-

- Short sellers along with the financial journalists are the actually only actors in the marketplace that are incentivized to ferret out fraud. I’ve called this the golden age of fraud … the fraud cycle follows the financial cycle with a lag.

- I suspect this cycle will be the granddaddy of them all when it comes to corporate bad behavior. My general rule of thumb is if Wall Street is offering it to you, you ought to be careful.

-

-

-

-

-

-

-

-

-

- I think that the changes that are underway today, and in particular the introduction of AI, render the world much less predictable than at any time, probably any time ever, and certainly any time in my lifetime.

- There is no asset that is so good that it can't become overpriced and lethal, and there are very few things that are so bad that they can't get cheap enough to be attractive.

- What AI basically does, I've come to realize, is it makes predictions. It doesn't answer questions. It makes predictions.

-

-

-

-

-

-

-

-

-

- What we are trying to do is look out five to seven years in the future and estimate what a company is worth then, and buy it at a big discount to that today.

- As terrible as the war is, it might affect one year’s cash flow a little bit; it doesn’t really alter the seven‑year business value very much.

- So much of the value today is in intangible assets, so we redo GAAP accounting to Oakmark accounting, and on our numbers we are looking for companies selling at a discount that are well managed and will grow value over time.

-

-

-

-